◎ A closer look at official data reveals a wobbly economy on the verge of crisis, and not solid “recovery” or healthy “growth.”

Updated on Jan. 24, 2021.

On Jan. 18, the PRC National Bureau of Statistics announced that China’s GDP grew 2.3 percent year-on-year to 101.6 trillion yuan ($15.6 trillion). The NBS also released data on food supply, industrial output, consumption, national investment in fixed assets, employment, incomes, and more areas which suggest that the Chinese economy is seeing a fast recovery from the novel coronavirus pandemic.

In comparison, the NBS announced a 6.0 percent GDP growth (98.65 trillion yuan) in 2019 on Dec. 30 that year. The figure represented a 0.1 percent decrease of 435 billion yuan from preliminary calculations.

Mainland media played up China’s official 2020 figures, reinforcing the Chinese Communist Party’s “all’s well” (形勢一片大好) propaganda messaging. Meanwhile, Western media outlets lauded China’s “economic recovery.”

Stimulus and debt-fueled growth

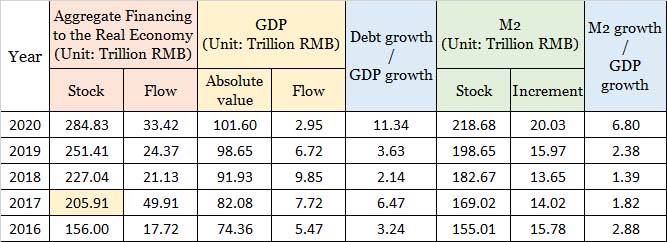

At the end of December 2020, China’s M2 money supply increased 20.03 trillion yuan to 218.68 trillion yuan, according to official data. This meant that the new money supply to GDP growth ratio was 6.8; that is, every 1 yuan of GDP growth was created by 6.8 yuan of central bank stimulus. In comparison, the M2 growth to GDP growth ratio was only 4.6 during the 2008-2009 period when the CCP released a 4 trillion yuan stimulus package to deal with the impact of the global financial crisis on the Chinese economy.

According to China Central Depository & Clearing data, the CCP regime issued 13.5 trillion yuan worth of bonds in 2020, an increase of 5.09 trillion yuan (+60.8 percent) from the previous year. Of the 13.5 trillion yuan of government bonds, 6.91 trillion yuan were issued by local governments, up 2.08 trillion yuan (+47.7 percent) from 2019. Meanwhile, the CCP regime’s fiscal revenue amounted to 16.95 trillion yuan in the first 11 months of the year and about 18 trillion yuan for the whole year (down 5 percent from 2019).

The stock of social financing in China in 2020 increased 33.42 trillion yuan from 2019 to 284.83 trillion yuan, according to People’s Bank of China data. However, China’s GDP growth was only 2.95 trillion yuan in 2020, which means that every 11.34 yuan of investment only generated 1 yuan of GDP growth (social financing stock/GDP growth).

China’s 284.83 trillion yuan social financing, a broad measure of credit and liquidity in the economy, generates an estimated annual interest of 14.24 trillion yuan if we calculate interest conservatively at 5 percent. In other words, China’s economic entities lost 11.3 trillion yuan in 2020, or 3.8 times the value of GDP growth.

The above data suggests that China’s growth in 2020 was largely fueled by the CCP regime issuing more debt and increasing stimulus. Such unhealthy, non-productive measures led to a false “economic recovery” for the PRC while compounding the regime’s systemic financial risks and debt crisis.

Fraudulent data

The CCP always manipulates its economic figures to make things look better than they really are. Data manipulation became especially obvious after the Sino-U.S. trade war commenced in 2018. For instance, the central government would order local statistical bureaus to stop publishing specific economic data and only issue overall growth rates. Meanwhile, growth is not measured according to simple year-on-year or month-on-month comparisons as in previous years, but according to an opaque “comparable caliber.” This allows CCP statisticians enormous leeway to manipulate data and produce statistically impossible “growth.” This “growth” and the perpetuation of the “China economic success story” is later “normalized” by PRC propaganda outlets and “taken at face value” reporting of official PRC economic data in Western media.

Table 1 shows a stark example of CCP data manipulation in recent years. In September 2018, the PBoC included local government special bonds in its calculation of total social financing, which is an indicator of financial support for the real economy. Concurrently, the PBoC revised its 2017 social financing stock data to 205.91 trillion yuan, up 31.2 trillion from the original figure of 174.71 trillion yuan.

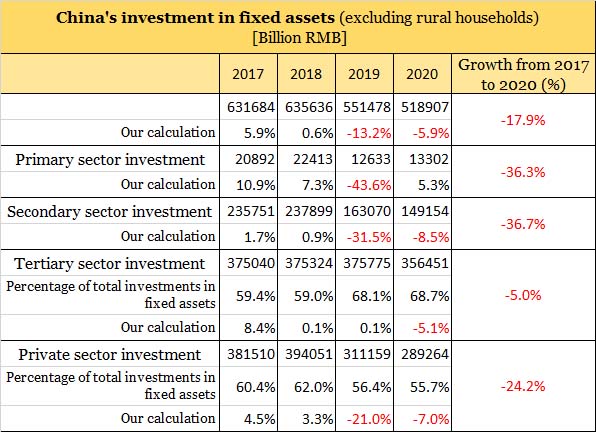

In Table 2, we use standard year-to-year comparisons to obtain China’s national fixed asset investment data for the years 2017 to 2020, and reveal the extent of the CCP’s data fraud and China’s economic deterioration. From our calculations, the CCP’s official fixed asset growth rate is significantly higher than actual growth rates starting from 2018, the year the Sino-U.S. trade war began. Sharp declines in 2019 and 2020 somehow becomes positive growth when looking at official figures. In particular, a 43.6 percent decline in primary industry investments in 2019 is announced as a 0.6 percent increase by the NBS at the time.

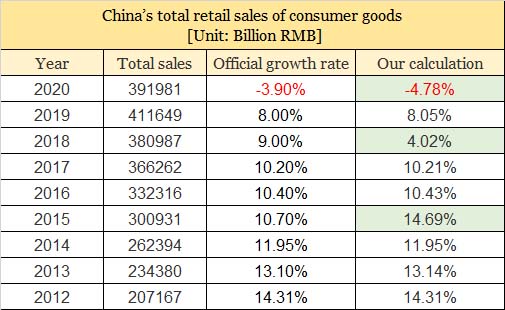

The CCP’s figures for total retail sales also show clear signs of falsification. A comparison of official NBS figures from 2012 to 2020 shows obvious differences in growth rates in three of the nine years. In particular, the official retail sales figure in 2015 and the one we calculated using a simple year-to-year comparison differs by nearly 4 percent.

The slowing of China’s growth drivers

The CCP and PRC economists always refer to a “troika” of growth drivers—consumption, exports and investment—when talking up China’s economic growth. The official CCP narrative after the release of the 2020 economic data of “recovery” is no different. A closer look at the “troika,” however, tells a different story.

Shrinking investments

Table Four shows that investments in China have shrunk sharply in the past four years. Part of the reason for this is the Sino-U.S. trade war and the coronavirus pandemic. Also, investors may not be optimistic about the state of China’s real economy. This means that the CCP will find it very challenging to grow the economy through more stimulus and debt measures alone.

From Table Four:

- China’s fixed asset investment growth for 2018 fell close to zero percent. That year, the U.S. levied the first tariffs on Chinese products.

- In May 2019, the U.S. imposed a third wave of tariffs, 25 percent on $250 billion worth of goods. By the end of 2019, China’s fixed asset investments fell to negative 13.2 percent, with investments in the primary industry taking the biggest hit (-43.6 percent).

- In 2020, China’s fixed asset investments fell 5.9 percent from the previous year on the whole, with only primary industry investments rebounding to 5.3 percent from a year ago after a precipitous decline in 2019.

- Between 2017 and 2020, China’s fixed asset investments fell by an astonishing 17.9 percent. This means that the CCP regime is far from returning China to the level of investments in 2017 despite its best efforts, while the private sector is less willing to make investments.

Coronavirus and U.S. exports

On Jan. 14, the PRC General Administration of Customs released China’s 2020 import and export data:

- The total value of China’s imports and exports increased 1.9 percent year-on-year in 2020 to 32.16 trillion yuan. Exports grew 4 percent to 17.93 trillion yuan, while imports decreased 0.7 percent to 14.23 trillion yuan. China’s trade surplus increased 27.4 percent to 3.7 trillion yuan.

- Calculated in U.S. dollars, the total value of China’s trade in goods in 2020 was $4.64 trillion, up 1.9 percent from a year ago. Exports increased 3.6 percent to $2.59 trillion, while imports decreased 1.1 percent to $2.06 trillion. The trade surplus grew 26.93 percent to $535 billion.

According to GAC data, China’s exports rose 3.6 percent to a record $2.6 trillion. While China’s trade surplus reached the second highest in the past decade ($535 billion), it was still about $60 billion less than the $594.5 billion in 2015.

China’s exports rose partly due to increased demand of China-made medical and computer products during the COVID-19 crisis, and partly due to foreign economies (particularly America) recovering slowly and releasing stimulus. According to customs data, China’s exported 438.5 billion yuan worth (about $67.5 billion using an exchange rate of 6.5) of personal protective equipment, or 12.6 percent of the total national trade surplus.

However, the appreciation of the renminbi in 2020 meant that many Chinese companies ended up losing money the more they exported. From a rate of 7.1316 on May 29, the RMB appreciated 8.53 percent to a high of 6.5236 to the U.S. dollar on Dec. 28. A strong RMB is bad news for traditional Chinese export companies, particularly those with a profit margin of less than 5 percent. Meanwhile, many overseas customers ended up delaying shipments and settlements due to the pandemic causing longer container turnaround time and increased shipping costs, factors which steepened the exchange rate losses incurred by Chinese export companies.

Meanwhile, China is still very dependent on the U.S. market for exports. In 2020, China’s trade surplus with America increased 7.1 percent from the previous year to $316.9 billion, accounting for 59.2 percent of the national trade surplus. China’s trade surplus with the U.S. in 2020 also rose 14.9 percent from 2017 ($265.8 billion). Even during the height of the trade war in 2019, China’s trade surplus with the U.S. was $295.8 billion.

Lower consumption

In May 2020, the CCP proposed the so-called “dual circulation” strategy to “leverage” China’s sizable domestic market to offset shrinking external demand. In theory, China’s “mega-scale markets” would be able to consume a portion of exports, which would be converted to “domestic sales,” thus allowing the CCP regime to become more “self-sufficient.”

However, China’s 2020 economic data suggests that its “dual circulation” policy is headed for failure:

- In 2020, China’s retail sales officially totaled 39.1981 trillion yuan, down 3.9 percent from the previous year (down 4.78 percent per our calculations). Sales of consumer goods other than automobiles fell 4.1 percent to 35.2566 trillion yuan for the year, with the steepest drop occurring during the January-February period (minus 20.5 percent).

- National consumer prices rose 2.5 percent in 2020 over the previous year. Food prices went up by 10.6 percent (with meat prices rising an astounding 38.4 percent), and non-food products rose by 0.4 percent (transportation and communications decreased 3.5 percent). In January, national consumer prices reached a peak of 5.4 percent.

- The national per capita consumption expenditure of Chinese residents decreased 1.6 percent nominally from a year ago to 21,210 yuan in 2020. After deducting price factors, the actual decrease was 4 percent.

- The national per capita disposable income of residents increased 4.7 percent nominally from the previous year to 32,189 yuan in 2020. After deducting price factors, the actual increase was 2.1 percent, lower than the 2020 GDP growth rate of 2.3 percent.

- The production and sales of passenger vehicles was 19.994 million (-6.5 percent YoY) and 20.178 million (-6 percent YoY) respectively in 2020, the third consecutive year of contractions in China’s auto market.

- In 2020, China shipped 307.9 million cellphone units, down 20.8 percent from a year ago.

Conclusion

The CCP maintains its rule at home and projects power abroad through lies, deception, and propaganda. A closer look at official data reveals a wobbly economy on the verge of crisis, and not solid “recovery” or healthy “growth.” The CCP’s stimulus and debt measures did help the Chinese economy regain some ground following the COVID-19 crisis, but at the cost of expanding China’s debt crisis and worsening systemic risks.

China’s economic prospects hinge on how quickly the Sino-U.S. relationship can “recover.” However, the Biden administration has signaled that it will prioritize domestic challenges early on, and is unlikely to undo the Trump administration’s tariffs (at least not completely) in the short term. In other words, the CCP regime still faces significant economic headwinds despite fortunes appearing to shift in its favor with political instability in the United States. The current trajectory of Sino-U.S. relations and the new coronavirus strain sweeping the world gives us reason to be skeptical about China’s economic prospects in the near future.