1 Analyzing Chen Yixin’s Qiushi piece on ‘enhancing natsec capabilities’

April 15 is observed annually as “National Security Education Day” in the PRC. Around this date, state media usually release reports and commentaries focused on national security themes. This April 15, the CCP Central Committee ideological journal Qiushi published a piece by minister of state security Chen Yixin titled, “Enhancing National Security Capabilities to Safeguard High-Quality Development” (提升護航高品質發展的國家安全能力).

Key points in Chen’s article include:

1. Coordinating development and security as a core governing principle.

- Security is the prerequisite for development, while development provides the foundation for security. High-quality development and high-level security should reinforce each other in a positive cycle.

- Safeguarding national security must be planned and implemented alongside economic and social development to ensure that national progress rests on a secure and reliable foundation.

2. The world is undergoing “profound changes unseen in a century,” with growing security deficits. Key challenges include:

- Great power competition and hegemonic pressure: Certain countries employ extreme pressure, trade wars, and technology wars.

- Sovereignty and territorial security: Issues involving Taiwan (opposition to “seeking independence through external support”), as well as external interference in affairs concerning Tibet, Xinjiang, and Hong Kong.

- Non-traditional security risks: Rising global terrorism, threats to overseas interests, and intensified espionage activities.

- Technology and resource competition: A new wave of technological revolution led by artificial intelligence has become a central arena of great power rivalry, with risks of “chokepoint” constraints.

3. More precise risk management and proactive positioning are required in a complex and evolving international environment. The article outlines six “major struggle” areas:

- Counter-subversion: Safeguarding political security and preventing “color revolutions.”

- Counter-hegemony: Opposing unilateralism and external suppression.

- Counter-separatism: Targeting “Taiwan independence” and other separatist forces.

- Counter-terrorism: Strengthening prevention at the source and protecting overseas interests.

- Counter-espionage: Cracking down on intelligence theft and enhancing risk control in emerging fields.

- Counter-blockade: Promoting technological self-reliance and breakthroughs in core technologies.

4. National security organs must strengthen four major capabilities:

- Risk early warning and prevention: Improve situational awareness and resolve risks at an early stage.

- Security maintenance and shaping: Shift from passive response to proactive anticipation and shaping.

- Strategic research capacity: Build world-class think tanks to enhance strategic judgment and planning.

- Institutional support capacity: Advance “eight major projects” (see below) to build a strong national security force.

5. Forge a “loyal, clean, and responsible” (忠誠乾淨擔當) national security force in the new era by systematically advancing the “eight major projects”:

- Theoretical innovation.

- Institutional reform.

- Technological empowerment (especially AI applications).

- Foreign-related work.

- New-type support.

- Rule-of-law development.

- Construction of a national security “iron force.”

- National security cultural construction.

The rise of the national security state under Xi

Building the national security state

After coming to power, Xi Jinping established the Central National Security Commission at the Third Plenum of the 18th Central Committee in 2013. The following year, Xi introduced the concept of the “holistic national security outlook,” with the objective of building a “centralized, unified, efficient, and authoritative” leadership system to ensure the Party’s absolute control over security affairs. This mechanism broke with the previous model under “collective leadership” by concentrating authority over national security, public security, foreign affairs, and economic governance in Xi’s hands. It also blurred the boundary between traditional security (such as military and territorial issues) and non-traditional security (such as economic, cultural, and technological domains), requiring all aspects of governance to adopt “bottom-line thinking” and “worst-case scenario thinking.”

Today, the underlying logic of all major economic and political decisions in China is rooted in this “holistic national security outlook.”

Post-20th Party Congress shift: From development-centered to security-prioritized governance

In 2022, the CCP authorities shifted from its reform-era model of having “economic development as the central task” to a framework of “coordinating development and security” (統籌發展與安全). Notably, the government work report presented at the 20th Party Congress devoted a standalone section to national security where the word “security” was mentioned 91 times. The sector emphasized the need to “build a new security architecture to safeguard a new development paradigm” and to prepare for “stormy seas” of external risks. This reflects Beijing’s heightened concern over so-called “Black Swan” and “Gray Rhino” events, as well as external “containment and blockade.”

Under the so-called “new era holistic national security outlook,” Beijing began to increasingly prioritize regime security in its governance. The Xi leadership has institutionalized security prioritization through legal revisions, bureaucratic restructuring, social mobilization, and foreign policy initiatives. The result is the construction of a comprehensive national security system spanning political, economic, technological, cyber, social, and emerging domains.

Legal expansion and rising compliance risks

The PRC has accelerated the development of its national security legal framework since the 20th Party Congress:

- The revised Counter-Espionage Law (2023) broadened the definition of espionage to include any data or activities related to “national security and interests.”

- The State Secrets Law (2024 revision) introduced the concept of “work secrets” and imposed tighter restrictions on the overseas travel of personnel with access to sensitive information.

- The Cybersecurity Law (2025 draft revision) strengthened oversight of artificial intelligence and critical infrastructure.

The ambiguity and expansive enforcement scope of these laws have created unprecedented compliance risks for multinational companies, affecting routine activities such as due diligence, cross-border data transfers, and talent mobility. One of the negative impacts of Beijing’s security prioritization is the increased “security premium” that the Chinese economy has to bear. In 2024, foreign direct investment to China fell 27.1 percent from a year ago, marking two consecutive years of steep declines. Surveys by European business groups indicate that the “politicization of the business environment” has become a top concern, prompting companies to accelerate “China+1” supply chain diversification and operational “decoupling.”

Institutional and social expansion of the security apparatus

Under Chen Yixin, the Ministry of State Security has sought to grant greater “public visibility” to national security issues, particularly in the fields of economics and finance. This reflects a shift in the MSS from being a traditionally covert intelligence body to a more visible actor actively involved in economic governance and public discourse management.

The Ministry of Public Security led by Wang Xiaohong has promoted digital identity systems such as unified online IDs and credentials. Meanwhile, national security education has been deeply embedded across the education system and public opinion management.

Externalization of security doctrine in foreign policy

The PRC has also projected its internal security framework outward through initiatives such as the “Global Security Initiative.” This includes positioning itself as a mediator in international conflicts, such as facilitating rapprochement between Saudi Arabia and Iran and promoting the “Beijing Declaration.”

In May 2025, Beijing released its first white paper on “National Security in the New Era,” reaffirming its firm stance on safeguarding core national interests.

Conclusion

The Xi leadership’s transformation of the PRC’s national security system after the 20th Party Congress is aimed at attaining “absolute security” for the regime. However, security prioritization has produced significant side effects, including declining economic dynamism, growing external trust deficits, and accelerating global supply chain restructuring. All in all, Beijing’s security-centric shift has become one of the most critical structural variables shaping China’s domestic development and its role in the international system today.

Our take

Chen Yixin’s piece in Qiushi appears to be the CCP’s response to economic and geopolitical troubles impacting the regime at the start of the 15th Five-Year Plan period. Amid worsening domestic and international conditions, Beijing is attempting to construct a more self-sufficient and security-centered system.

1. Chen’s article points to the further institutionalization of Xi Jinping’s “holistic national security outlook,” with centralization in the name of regime security becoming more refined and operationalized.

For instance, the article calls for consolidating a “centralized, unified, efficient, and authoritative” national security leadership system, alongside “systematic reform projects” to optimize vertical management. This implies that local branches of the Ministry of State Security will increasingly report directly to the central government, rather than being constrained by local governments’ short-term economic priorities. This restructuring is designed to enable rapid nationwide mobilization of resources — particularly in response to external shocks such as President Donald Trump’s sharp tariff escalation against China in early 2025 — without interference from local concerns over foreign investment outflows.

Chen’s article also reflects a proactive expansion of the MSS’s functions. It redefines national security capability as encompassing both “defending” (維護) and “shaping” (塑造) security. The concept of “shaping security” marks an important shift, namely, that the PRC is no longer positioning itself as a passive recipient of external pressure, but as an active architect of its environment. This includes moves like rule-setting (e.g., data governance frameworks), intensified enforcement (e.g., counter-espionage measures), and active countermeasures (e.g., export controls on critical resources such as rare earths). The MSS’s functional expansion is particularly evident in initiatives such as the “rule-of-law construction project” and “technology empowerment project,” which undergird the security authorities’ move to leverage AI and legal instruments to build comprehensive monitoring systems across both digital and physical domains.

2. The six areas of “major struggle” that Chen Yixin identifies in his article highlight where Beijing’s security priorities are for the 15th Five-Year Plan period (2026 to 2030).

i) Counter-subversion is placed first, reflecting Beijing’s heightened concerns over regime security. The emphasis on preventing “color revolutions” and “street politics” reflects Beijing’s concerns that economic slowdown and rising unemployment could lead to political instability.

ii) Counter-hegemony directly corresponds to structural tensions in the Sino-U.S. relationship. The CCP authorities have been increasingly calling out Washington’s actions as “hegemonism,” including Trump’s 2025 “Liberation Day” tariffs and the U.S. war on Iran. Meanwhile, Chen Yixin’s call to resist “long-arm jurisdiction” and “technological blockade” indicate that the CCP is looking to build alternative systems that are less dependent on the U.S. dollar and American technology ecosystems.

iii) Counter-separatism is closely linked to issues involving Xinjiang, Tibet, and Taiwan. Beijing’s answer to the Taiwan issue to adopt the posture of extreme military pressure (the frequency of PLA incursions into Taiwan’s Air Defense Identification Zone in 2025 reached 3,764 sorties, an increase of over 18,700 percent compared to 2019) to display what Chen describes as the PRC’s “capability to shape security actions” with an eye on deterring “Taiwan independence” and external interference.

iv) Counter-espionage and counter-blockade are linked to the PRC’s economic transition. In his piece, Chen called for “counter-espionage struggles” to combat the theft of secrets and “counter-blockade struggles” to achieve technological self-reliance and strength. The CCP’s 15th Five-Year Plan also identifies the need to resolve “chokeholds” as a primary mission.

These “struggles” collectively reflect a fundamental shift. The PRC increasingly views economic activity as part of a broader “total struggle” framework. Trade is no longer merely about exchange, but serves as both a “lever” and a “shield” in geopolitical competition. This mindset was demonstrated in 2025 when Beijing implemented rare earth export restrictions against Japan in response to the Sanae Takaichi administration’s November 2025 remarks regarding Taiwan.

3. The “eight major projects” outlined by Chen Yixin reveal how the PRC national security apparatus plans to use technological tools to deepen the CCP’s surveillance and control over Chinese society and the economy.

Technology empowerment

This project emphasizes the use of AI to guide the development of integrated “network–data–intelligence” systems to upgrade the CCP’s digital authoritarianism.

Previously at the 2026 “Two Sessions,” the National Development and Reform Commission explicitly proposed building a “self-reliant AI ecosystem.” For the MSS, this implies embedding automated monitoring and early-warning mechanisms into financial transactions, social media platforms, and cross-border communications. As Chen noted, the goal is to neutralize risks while still in their “incipient stage.”

Cultural construction

In his article, Chen called for showcasing the “distinctive mystique, wonder, and sanctity” of national security organs while fostering a social atmosphere in which “everyone safeguards national security.” Through cultural engineering, practices like public reporting (i.e. people reporting on each other) and vigilance toward “foreign influence” are being internalized as everyday behavioral norms. This not only increases the difficulty for foreigners to travel and work in China, but also deepens barriers to people-to-people exchange between China and the outside world.

“Iron force” construction

For the Xi leadership, ensuring the loyalty of coercive state organs like the MSS is a top priority amid economic slowdown and fiscal strain. Therefore, national security workers need to be “resolute and incorruptible, providing peace of mind to the Party” (堅定純潔、讓黨放心), as Chen emphasized in his article.

Internal discipline-building is intended to ensure that, in operations such as the 2025 crackdowns on due diligence firms, personnel remain aligned and unaffected by external pressure or material incentives.

4. In sum, Chen Yixin’s article makes clear that economic activity in China is no longer treated as an independent objective of growth, but as an instrument serving “political security” and “counter-blockade” goals. This shift has already been institutionalized in the CCP’s 15th Five-Year Plan.

However, the economic costs of this broad securitization are increasingly evident. The first annual decline in fixed asset investment in 2025 (negative 3.8 percent) and the continued contraction of foreign direct investment quantitatively demonstrate the price of prioritizing security over economic development. Capital risk aversion and the stagnation of private investment now represent the greatest threats to the Chinese economy.

Furthermore, the PRC’s emphasis on “counter-hegemony” signals that the regime’s relations with the United States have “stalemated.” Looking ahead, U.S.-China confrontation in the technological and financial sectors will become the norm and supply chain de-risking will become irreversible.

U.S.-China relations have entered a ‘long-term stalemate,’ where confrontation in the technological and financial sectors will become the norm and supply chain de-risking has become irreversible. If national security reviews continue to expand into general commercial cooperation and academic exchange, the bilateral “decoupling” will spread from high-tech sectors into broader areas of everyday economic and social interaction.

Beijing’s over-generalization of national security is causing international investors to view the country as having transformed from an “opportunity-driven” market into a “rules- and geopolitics-driven” market. The CCP’s national security apparatus is firmly at the helm in navigating the regime through “stormy seas” of domestic and international turbulence. Understanding Chen Yixin’s framework of the “six major struggles” and “eight major projects” may now be more important to figuring out China’s economic direction than interpreting fiscal or economic reports. Over the next five years, China’s policy balance is likely to continue tilting toward security, or until mounting structural economic pressures and social constraints force another round of policy adjustment.

2 China’s Q1 2026 data shows structural rift between external boost and domestic slump

On April 16, the PRC National Bureau of Statistics released China’s economic data for the first quarter and March. The NBS claimed that the Chinese economy achieved a “good start” to the year under the “strong leadership of Party Central with Comrade Xi Jinping at the core,” with developmental resilience and vitality further demonstrated.

Key data include:

GDP

- Q1 2026 GDP: Preliminary estimate of 33.4193 trillion yuan, up 5.0 percent year-on-year (in real terms) and 0.5 percentage points faster growth than Q4 2025. Quarter-on-quarter growth of 1.3 percent.

- Industrial structure:

- Primary industry: Up 3.8 percent to 1.1941 trillion yuan.

- Secondary industry: Up 4.9 percent to 11.6135 trillion yuan.

- Tertiary industry (services): Up 5.2 percent to 20.6117 trillion yuan.

Industrial production and energy

- Value added of industrial enterprises above designated size:

- Q1 2026: Up 6.1 percent year-on-year.

- March 2026: Up 5.7 percent year-on-year, up 0.28 percent month-on-month.

- Sector brightspots:

- Electronics and information: Up 13.6 percent year-on-year.

- Electrical machinery: Up 7.3 percent year-on-year.

- Overall manufacturing: Up 6.0 percent year-on-year.

- Energy production:

- Electricity generation: Up 3.4 percent year-on-year in Q1 2026.

- Natural gas: Up 3.0 percent to 23.4 billion cubic meters in March 2026.

- Crude oil: Up 1.3 percent to 54.8 million tons in Q1 2026.

Fixed asset investment

- Total (excluding rural households): Up 1.7 percent year-on-year to 10.2708 trillion yuan.

- Breakdown:

- Infrastructure: Up 8.9 percent year-on-year.

- Manufacturing: Up 4.1 percent year-on-year.

- Primary sector: Up 15.9 percent year-on-year.

- Private investment: Down 2.2 percent year-on-year.

Consumption and household income

- Retail sales of consumer goods:

- Q1 2026: Up 2.4 percent year-on-year to 12.7695 trillion yuan.

- March 2026: Up 1.7 percent year-on-year to 4.1616 trillion yuan.

- New consumption trends: Online retail up 8.0 percent year-on-year, with physical goods accounting for 24.8 percent of total retail sales.

- Household income and spending:

- Per capita disposable income: 12,782 yuan, up 4.9 percent nominal, up 4.0 percent real.

- Per capita consumption expenditure: 7,955 yuan, up 3.6 percent nominal, up 2.6 percent real.

Real estate market

- Real estate development investment: Down 11.2 percent year-on-year to 1.772 trillion yuan.

- Commercial housing sales:

- Floor space sold (195.25 million sqm): Down 10.4 percent year-on-year.

- Sales value (1.7262 trillion yuan): Down 16.7 percent year-on-year.

- Housing prices (70 major cities, March 2026): The market shows a “divergence” of month-on-month improvement but year-on-year weakness.

- Tier-1 cities:

- New homes: Up 0.2 percent month-on-month (from flat previously).

- Second-hand homes: Up 0.4 percent month-on-month (from negative 0.1 percent previously).

- Cities like Beijing (up 0.6 percent month-on-month for second-hand homes) and Shanghai show strong resilience.

- Tier-2 cities:

- New home prices down 0.2 percent month-on-month.

- Tier-3 cities:

- Down 0.3 percent month-on-month, with no meaningful narrowing of declines.

- Housing price trends in March 2026 suggest that capital and demand are increasingly concentrated in core cities, while non-core cities face severe liquidity constraints.

- Despite month-on-month improvements, year-on-year declines remain significant. This indicates that current housing prices remain well below last year’s levels, and the market has yet to recover from the earlier downturn:

- Tier-1 second-hand housing: Negative 7.4 percent year-on-year.

- Tier-2 cities: Negative 6.2 percent year-on-year.

- Tier-3 cities: Negative 6.4 percent year-on-year.

Our take

The CCP has been talking up China’s latest economic numbers, with state media promoting the narrative of “strong resilience” and “vibrant dynamism” amid global instability. However, a closer examination of the official data — stripped of statistical embellishment and analyzed at a structural level — reveals a substantial disconnect between the reported 5 percent GDP growth and underlying economic conditions. Beneath the facade of prosperity, weakening consumption, a hard landing in the property sector, deteriorating local government finances and the risk of a high-tech investment bubble are converging.

1. Beijing’s official GDP growth rate of 5.0 percent sits at the upper bound of the official target range of 4.5%–5.0%. Yet beneath this headline figure, key indicators of the real economy display clear weakness and inconsistency.

In considering the expenditure approach to GDP (consumption, investment, and net exports), the growth rates of retail sales (up 1.7 percent) and fixed asset investment (up 1.7 percent) are insufficient to produce the overall growth rate of 5.0 percent unless government spending or inventory accumulation has expanded in an unusually large and non-market-driven manner.

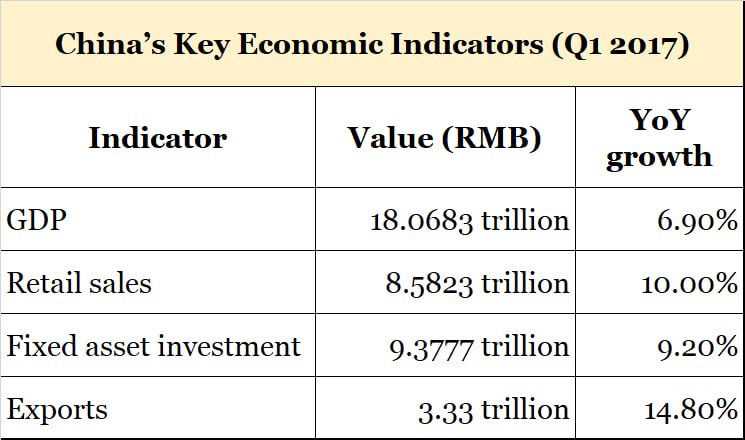

A comparison with the pre–trade war period illustrates this divergence:

In contrast to 2026, the key demand-side indicators in 2017 were all growing significantly faster than GDP, reflecting a more balanced and demand-driven expansion.

The current statistical divergence highlights the increasingly asymmetric nature of China’s growth model. Growth momentum is concentrated in high-tech manufacturing driven by AI infrastructure investment and select export demand linked to geopolitical disruptions, particularly those associated with the Iran conflict. Meanwhile, sectors critical to household welfare and long-term growth — private investment, real estate, and mass consumption — are experiencing deep and prolonged contraction.

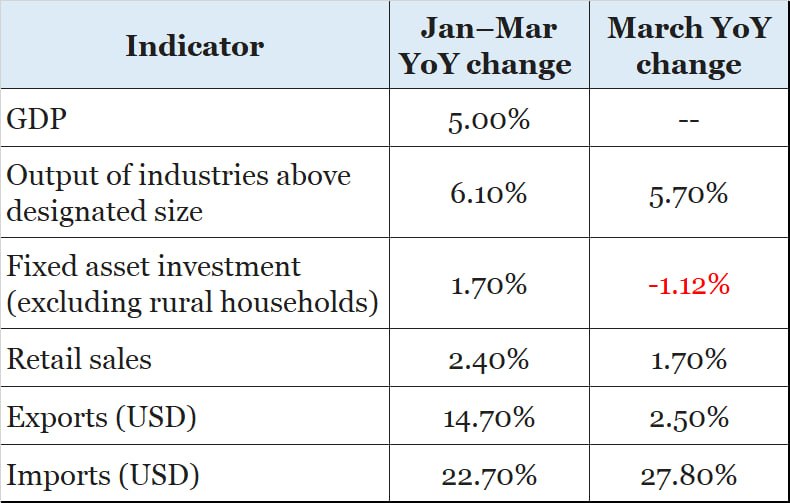

The table below compares the divergence between key macroeconomic indicators and GDP growth in the first quarter of 2026:

The above table shows that the gap between the supply side (industrial production) and the demand side (consumption and investment) has widened to historically elevated levels. The resulting “strong production, weak domestic demand” pattern represents a K-shaped divergence, in which excess or inefficient supply is used to mask the erosion of endogenous demand. When state-driven production becomes decoupled from market-based consumption, China’s economic “good start” increasingly resembles a form of government-sustained growth rather than a reflection of genuine economic vitality.

2. China’s value-added industrial output above designated size grew by 6.1 percent year-on-year in Q1 2026, emerging as the sole “peak” supporting GDP growth. However, a closer examination of sectoral data reveals that this expansion is not driven by domestic consumption upgrading or a recovery in traditional industries, but is highly dependent on specific external stimuli.

i) Global investment in AI infrastructure intensified significantly at the beginning of 2026. In March, integrated circuit output rose 20.6 percent year-on-year, industrial robot production increased 24.4 percent, and value-added in computer, communications, and electronic equipment manufacturing grew 12.5 percent. As a major global hub for server components, semiconductor packaging, and electronics manufacturing, China experienced a surge in related output and exports.

Despite continued U.S. restrictions on advanced AI chips and tariff pressures, Chinese firms have boosted industrial performance by expanding market share in mature-node manufacturing and assembly segments. This growth, however, exhibits low employment elasticity. While high-tech manufacturing raises output figures, its highly automated production processes fail to absorb surplus labor displaced by the real estate downturn. This has resulted in a divergence characterized as “industrial strength alongside weak household conditions.”

ii) Geopolitical developments have also provided temporary demand support. As the Iran conflict extended into its seventh week, global demand for transportation equipment and specific electronic components surged due to wartime attrition and precautionary procurement. Investment in railway, shipbuilding, aerospace, and related sectors rose 27.7 percent in Q1 2026, while sectoral value-added increased 13.3 percent in March.

The “war dividend” that China has been enjoying, however, is rapidly turning into a cost burden. Disruptions in shipping routes, particularly around key maritime chokepoints, have driven up global energy prices, significantly increasing China’s import costs. In March, imports surged 27.8 percent, largely driven by stockpiling of energy and critical minerals. As a result, China’s trade surplus narrowed sharply to $51.13 billion, less than half the average level of the previous two months. This indicates that short-term resilience in external demand is being offset by margin compression caused by imported inflation.

3. If manufacturing represents the “visible strength” of the Chinese economy, then the 1.7 percent growth in retail sales in March reflects its underlying fragility. The broad-based contraction in consumption highlights weak income expectations and balance sheet adjustments by households.

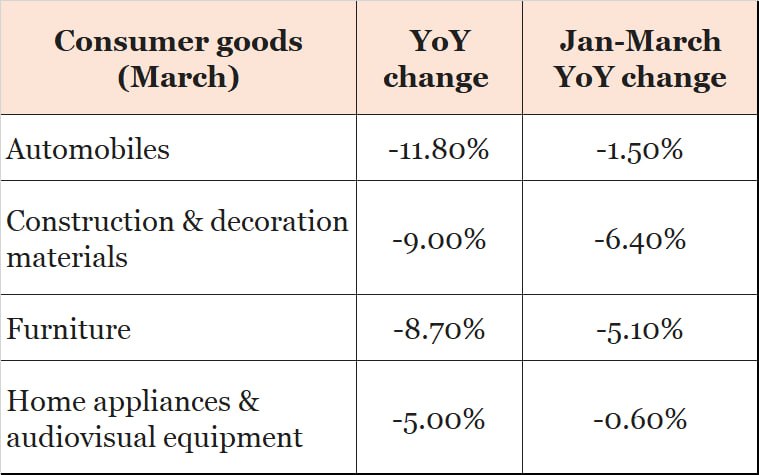

i) Apart from communications equipment (up 27.3 percent, driven by AI-related demand) and gold and jewelry (up 11.7 percent, reflecting safe-haven behavior), most durable consumer goods linked to middle-class living standards declined sharply in Q1 2026:

The 11.8 percent decline in auto sales is particularly significant. Even with government incentives such as trade-in programs, Chinese households remain reluctant to take on large credit obligations. This reflects not merely a shift in consumption preferences, but the disappearance of the wealth effect. With housing assets no longer appreciating and youth unemployment remaining elevated, households are prioritizing cash accumulation over leverage.

ii) Persistent declines in construction-related consumption categories directly reflect the spillover effects of the real estate downturn. Delays in housing delivery and stagnation in secondary market transactions have undermined demand for appliances and building materials.

At the same time, consumption patterns are becoming more defensive. For instance, convenience store sales saw 8.3 percent growth, department store sales dropped 0.1 percent, and specialty retail chain sales declined 4.2 percent. This shift from higher-end consumption to basic necessities indicates a trend of consumption downgrade.

4. China’s real estate downturn has now entered its sixth year, and the Q1 2026 data suggests that the contraction is not only ongoing but potentially accelerating. Real estate development investment fell by 11.2 percent, with the rate of decline widening compared to the beginning of the year. This suggests that the industry’s liquidity crisis has evolved into a systemic loss of confidence.

The performance of leading housing indicators is dismal. From January to March, new housing starts plummeted by 20.3 percent year-on-year, with residential starts down 22.0 percent. This means developers have essentially halted all new expansion plans, focusing entirely on completing existing projects or debt restructuring. Yet even in the government-prioritized area of project delivery, completed housing area fell by 25.0 percent. This breakdown at the completion end will further erode buyer confidence, creating a vicious cycle: fear of buying → capital exhaustion → inability to complete construction → increased fear of buying.

Funding for real estate developers fell by 17.3 percent in the first quarter, a reflection of continued property sector troubles. The indicator most reflective of market sentiment — personal mortgages — plunged by 34.6 percent, while deposits and down payments fell by 20.1 percent. These figures demonstrate that residents are actively fleeing mortgage debt even with bank interest rates at historic lows. Also, the 23.7 percent drop in domestic loans reveals that financial institutions’ risk aversion toward real estate has reached its limit.

According to March data for 70 large and medium-sized cities, falling house prices have become a universal trend rather than an isolated phenomenon:

- New commercial housing: Prices fell month-on-month in 49 out of 70 cities (about 70 percent).

- Second-hand homes: 48 cities saw price drops, with significant declines in provincial capitals and major economic hubs such as Luoyang, Wuhan, and Nanning.

S&P Global predicts that total sales of new commercial housing will fall by another 10%–14% for the full year of 2026. This implies that the wealth transfer mechanism upon which China’s economic growth relied for the past twenty years has effectively broken down. The exhaustion of land-based finance will, in turn, severely restrict the investment capacity of local governments.

5. China’s fixed asset investment grew by only 1.7 percent in the first quarter, with a severely imbalanced internal structure. Meanwhile, investment by state-controlled entities rose 7.1 percent, while private fixed asset investment declined 2.2 percent. This statistical gap represents a systemic shift in the power structure of the Chinese economy.

i) Amid a broad retreat by the private sector, the CCP authorities have relied on state-owned enterprises to push infrastructure investment (up 8.9 percent), particularly in aviation (up 43.3 percent) and water transport (up 34.1 percent). However, the marginal returns on such debt-financed projects are rapidly diminishing. Much of the investment is directed toward low-density regions or state-led industrial projects already facing overcapacity, creating substantial long-term financial burdens.

ii) Fixed asset investment by foreign-invested enterprises fell 6.3 percent in Q1 2026, while investment from Hong Kong, Macau, and Taiwan declined 5.0 percent. This is a continuation of the record-breaking FDI outflows seen in 2025, and a sign that international capital has shifted its perception of the Chinese market from “indispensable” to “risk-averse.” The contraction in private investment (negative 2.2 percent) is particularly critical as it signifies the shrinking of the typically most efficient and job-creating segment of the Chinese economy. Nomura Securities noted that without a recovery in private investment, any growth supported by government debt is unsustainable and illusory.

6. External trade, once regarded as a key stabilizer of China’s economy in 2025, is showing signs of deterioration. Export growth decelerated sharply from 21.8 percent at the start of the year to 2.5 percent in March, falling well below market expectations. This suggests that international demand is no longer able to reliably offset domestic weaknesses (see here for more analysis).

7. First-quarter financial data released by the People’s Bank of China further illuminate the internal mechanisms behind the economic slowdown. Total social financing increased by 14.83 trillion yuan, or 354.5 billion yuan less than a year earlier. Meanwhile, broad money (M2) grew 8.5 percent and narrow money (M1) rose just 5.1 percent. This widening gap indicates that liquidity is accumulating within the banking system rather than circulating into the real economy. Also, while RMB loans increased by 8.6 trillion yuan in Q1 2026, the bulk of these funds was directed toward debt rollover for state-owned enterprises and extensions for government infrastructure projects rather than new productive activity.

Within the stock of social financing, government bonds accounted for 21.6 percent (up 1.5 percentage points year-on-year) while corporate bond issuance and equity financing shares declined. This demonstrates that China’s financing system is increasingly reliant on sovereign credit. The International Monetary Fund projects that China’s general government debt will exceed 102 percent of GDP in 2026. Under conditions where nominal GDP growth lags real growth (i.e., deflation), this debt-dependent model becomes particularly fragile.

8. China’s producer price index turned positive in March 2026 (up 0.5 percent year-on-year), ending a 41-month period of decline. However, this shift was driven not by domestic demand recovery but by imported inflation stemming from higher global energy prices. On a quarterly basis, PPI still declined 0.6 percent from a year ago.

The combination of rising producer prices (up 0.5 percent) and weak retail sales growth (up 1.7 percent) creates severe margin compression. Upstream input costs increased (purchase prices: up 0.8 percent year-on-year, up 1.2 percent month-on-month), while downstream demand remains too weak to absorb price increases. As a result, profit margins in mid- and downstream manufacturing sectors are being squeezed, limiting firms’ capacity to raise wages or expand employment. This reflects an unusual coexistence of deflationary demand conditions and cost-push inflation.

9. Our assessment of China’s official Q1 2026 data yields several conclusions:

- Hollowing out of growth quality: The 5.0 percent GDP growth rate is largely a construct woven together by AI-related investment, conflict-induced export demand, and government debt expansion. Once these exogenous stimuli are removed, the core of the Chinese economy — consumption and private investment — is teetering on the edge of near-zero growth.

- Real estate ‘gordian knot’: The property sector has entered a mathematical “gravity field.” Conventional monetary policies (such as interest rate cuts or lower down payments) are no longer capable of reversing a structural downturn driven by a shrinking population and damaged balance sheets.

- The fragility of the ‘external circulation’: The U.S.-Iran war has exposed the vulnerability of China’s strategy of relying on exports to alleviate domestic overcapacity. High energy and transportation costs are rapidly offsetting the cost advantages of Chinese manufacturing, with the export slump in March likely marking the beginning of a broader trend.

- The exhaustion of policy tools: The rapid expansion of government debt is approaching critical thresholds, while the room for interest rate cuts is constrained by exchange rate pressure and narrowing net interest margins (NIM) for banks. Research reports from Goldman Sachs and Nomura indicate that the April Politburo meeting is unlikely to produce any significant stimulus. This means the economy will continue to slide along a track characterized by low growth, high debt, and persistent deflationary pressure.

Looking ahead to the remaining quarters of 2026, the Chinese economy will likely face even harsher tests. If the collapse of internal demand further resonates with external conflicts, maintaining a 5 percent GDP growth figure will require even larger-scale “technical processing” of statistics or more aggressive state-driven investment.

Global investors and observers should recognize that China’s era of high-speed growth driven by real estate and cheap manufacturing has ended. This model has been replaced by a structurally weaker, less transparent economic environment characterized by elevated geopolitical risk and diminishing growth sustainability.