1 Orbán’s defeat deals blow to the CCP’s European ambitions

Hungarians oust Orbán

On April 12, Hungarians turned out in record numbers to vote out incumbent prime minister Victor Orbán and end his 16-year rule.

Data released by the Hungarian National Election Office on election night and in the early hours of the following day showed that Péter Magyar’s Tisza Party (Respect and Freedom Party) won 138 out of 199 parliamentary seats, granting it a supermajority to amend the constitution. In contrast, Orbán’s Fidesz Party (Hungarian Civic Alliance) obtained only 55 seats while the Mi Hazánk Party (Our Homeland Movement” won 6 seats.

Hungary — the PRC’s strategic foothold in Eurasia

Under Viktor Orbán, Hungary pursued an “Eastern Opening” policy that positioned the European Union and NATO member as a strategic hub connecting eastern and western capitals, technology, and logistics. This strategy aligned closely with the PRC’s Belt and Road Initiative.

In May 2024, Xi Jinping paid a state visit to Hungary, during which the two countries elevated their relationship to a “comprehensive strategic partnership for all-weather cooperation in the new era” (新時代全天候全面戰略夥伴關係). This makes Hungary a strategically invaluable “foothold” for Beijing within the EU and a “testing ground” for the PRC’s external plans amidst global shifts.

Hungary has long played the role of “buffer” and “vetoer” within the EU. Budapest has repeatedly obstructed EU attempts to issue critical statements against Beijing regarding human rights, Hong Kong, and the South China Sea. Hungarian foreign minister Péter Szijjártó has also explicitly protested NATO’s labeling of China as a “systemic challenge,” emphasizing that Hungary does not wish for NATO to evolve into an anti-China bloc. In May 2025, deputy foreign minister Levente Magyar stated that Hungary will not “decouple” from China even if pressured by the U.S., viewing this as a “red line.” Hungary’s stance on the PRC has raised concerns within the EU and NATO that the country is serving as a “Trojan horse” for China.

Hungary is currently the largest recipient of Chinese foreign direct investment in the EU, attracting approximately $18 billion between 2014 and 2025. The small nation of 9.5 million people is also the world’s second-largest destination for Chinese electric vehicle manufacturing investment, trailing only Indonesia.

Bilateral trade between China and Hungary has doubled over the past decade, reaching $16.2 billion in 2024. Although the trade balance leans heavily toward China (with Hungary exporting roughly $1.86 billion against over $11 billion in imports), the Hungarian government prioritizes its long-term strategic gains as a regional logistics hub.

Hungary is also striving to become a regional financial center, which means that it would serve as a “bridgehead” for Chinese financial institutions entering Europe. Currently, four of China’s five major state-owned banks have established a significant presence in Budapest.

Meanwhile, the PRC’s footprint in Hungary has expanded far beyond economic cooperation, reaching into the underlying architecture of national security and education.

- In 2023, Hungarian tech giant 4iG signed an agreement with Huawei to co-develop cloud services and artificial intelligence centers. This includes not only telecommunications infrastructure but also AI-driven facial recognition applications potentially used for monitoring political protests.

- In February 2024, an agreement allowed Chinese and Hungarian police to conduct “joint patrols” in tourist hotspots and crowded areas like Budapest.

- Fudan University had planned to establish its first European campus in Budapest’s 9th District, with an estimated investment of $1.5 billion. However, the project is effectively on hold due to electoral pressures in 2026 and fiscal constraints.

Our take

1. Victor Orbán’s defeat means Beijing has lost a key “foothold” in Europe. If the PRC cannot cultivate other proxies, its strategy of undermining EU efforts at “de-risking” from China and expanding PRC influence in Europe through selective state-level influence is in danger of collapse.

For over a decade, the Orbán government effectively functioned as a “proxy” for PRC interests in Brussels. Utilizing the EU’s “unanimity rule,” Hungary has repeatedly defused diplomatic and geopolitical crises for Beijing at critical junctures. A sampling of EU initiatives blocked or diluted during Orbán’s tenure includes:

- Under Orbán, Hungary vetoed China-related motions at the EU Council level at least six times.

- In 2017, the Orbán government refused to sign a petition condemning the torture of human rights lawyers in China.

- In 2021, the Orbán government blocked three consecutive EU statements criticizing China’s crackdown on Hong Kong’s democracy.

- The Orbán government consistently opposed defining China as a “systemic challenge.” This helps Beijing carve out crucial strategic space in Europe amidst intensifying U.S.-China competition.

With Orbán’s departure, Beijing loses what amounted to a de facto “veto lever” capable of obstructing EU-wide China policy, including trade sanctions and strategic reviews.

2. Péter Magyar and his Tisza Party campaigned on promises of a “return to European values” and “clearing out corruption.” Assuming they follow through on campaign promises, Magyar and his party will inevitably upend Beijing’s interests and influence in Hungary. Based on these commitments, Hungary’s future policy trajectory is likely to impact China across multiple dimensions:

- Magyar repeatedly emphasized “accountability” and “transparency,” pledging to expose “what was left behind by those in power.” He committed to reviewing all “secret international agreements” and classified documents signed under Orbán. This would directly affect Chinese-funded projects such as the Hungary–Serbia railway, which had been designated as state secrets for ten years.

- Magyar pledged to join the European Public Prosecutor’s Office. This implies that Chinese-funded infrastructure projects involving EU funding or regulatory frameworks would be subject to EU-level judicial scrutiny. Beijing’s preferred opaque, government-to-government financing model would be exposed under rule-of-law oversight.

- Magyar’s foreign policy team has stated that Hungary should no longer act as a “stick in the wheel,” but rather as a “spoke in the wheel.” This signals several shifts unfavorable to Beijing:

- Hungary would abandon Orbán’s rhetoric of “economic neutrality” and instead support the EU’s trade defense instruments against China. Chinese firms would no longer enjoy quasi-extraterritorial advantages in Hungary.

- Ending rule-by-decree governance would significantly raise legal and regulatory costs for Chinese companies such as BYD and CATL, which had relied on informal arrangements with centralized authority for land acquisition and environmental approvals.

- Magyar has framed China as a “global power to be approached with caution,” rather than a partner of “ironclad friendship.” His support for Ukrainian sovereignty and efforts to reduce dependence on non-allied countries for energy could further weaken China’s “14+1” cooperation framework in Central and Eastern Europe. As public distaste for “crony capitalism” turns into strict audits of Chinese projects, Beijing’s painstakingly constructed political-economic integration in Hungary faces a comprehensive review, restructuring, and potential rollback.

3. Beijing’s agenda within the EU could be significantly constrained if the new Hungarian government pursues comprehensive audits and anti-corruption actions across three core sectors, namely, infrastructure, advanced manufacturing, and the financial system.

Infrastructure

The Budapest-Belgrade Railway, Beijing’s most ambitious Belt and Road flagship project in Central and Eastern Europe, is at risk of being transformed from a strategic asset into a legal and technical burden under the Magyar government.

As of early 2026, the Hungarian section remains in a state of “technical paralysis,” running only one train per hour because the Chinese-provided ETCS (European Train Control System) has not been authorized. The Magyar government could reject any “Chinese technical compromises” that do not meet EU standards, forcing the PRC to either bear substantial retrofitting costs or face indefinite delays.

Magyar has pledged to publicize secret loan agreements associated with the project totaling €2.5 billion. Transparency on the issue will expose the CCP’s “debt-leverage infiltration” model. If an audit uncovers cronyism involving Orbán’s inner circle, the new government may follow precedents seen elsewhere by renegotiating contracts or initiating partial default investigations.

Advanced manufacturing

Beijing had intended to position Hungary as a “Made in Europe” manufacturing base to bypass EU tariffs. However, under Magyar, Chinese firms may face rising costs due to stricter compliance with EU law.

Companies such as BYD and CATL previously benefited from land acquisition and environmental exemptions granted under Orbán’s emergency decree system. Under the new government, previously revoked permits — such as CATL’s disaster recovery authorization — could face renewed judicial scrutiny.

In addition, the EU’s proposed Industrial Acceleration Act, which requires 70 percent of components (excluding batteries) to be produced within the EU, could be used by the Magyar government to eliminate state subsidies for Chinese firms. This would prevent companies from obtaining EU origin status through simple assembly, undermining Beijing’s strategy of “repackaging” exports for entry into the European market. The Magyar government could also restrict plans to have those products manufactured in neighboring Serbia and then assembled in Hungary for tariff-free access to the EU.

Financial system

Magyar’s stated goal of joining the eurozone by 2030 could disrupt Beijing’s ambition to develop Budapest as an offshore renminbi hub.

If Hungary aligns with the eurozone, its financial system will fall under the direct supervision of the European Central Bank. This would subject existing high-volume, low-transparency RMB clearing operations in Budapest (which reached 555.7 billion yuan in 2024) to stringent anti-money laundering and sanctions compliance reviews.

A shift toward eurozone integration would likely marginalize the renminbi in bilateral settlement, depriving Beijing of a key foothold within the EU for bypassing the eurodollar financial system and promoting currency internationalization.

Chinese investments are already deeply embedded in Hungary’s economy (such as CATL’s battery plant), making a full “decoupling” unlikely. However, the new government’s emphasis on transparency, removal of political veto mechanisms, and realignment with EU policies could significantly narrow China’s ability to dump goods or circumvent regulatory frameworks within the EU.

4. The political shift in Hungary marks the beginning of a “cold winter” of low growth, high risk, and strict regulation for Beijing’s global expansion strategy. Hungary’s pivot could come to reflect a broader European reassessment of security and sovereignty vis-à-vis the PRC.

For the CCP regime that is driving towards global hegemony, the loss of Budapest as a reliable partner effectively closes a key gateway into Europe’s core. Unless Beijing can find new proxies, it faces an increasingly isolated position in Europe in the coming years.

2 China’s March 2026 trade data hints at stalling exports engine

China’s official Q1 trade data

April 14

PRC state media reported “strong opening” trade data for the first quarter of 2026.

- China’s total imports and exports increased 15 percent year-on-year to reach 11.84 trillion yuan. The quarterly total exceeded 11 trillion yuan for the first time, while the growth rate hit a five-year high.

- Total trade remained above 10 trillion yuan for 12 consecutive quarters, with growth returning to double digits since Q4 2022.

- Trade with key regions expanded broadly:

- Trade with ASEAN countries and Latin America both rose by 15.4 percent.

- Trade with Africa increased by 23.7 percent.

- Trade with the European Union and the United Kingdom grew by 14.6 percent and 13.1 percent respectively. These gains effectively offset the decline in trade with the United States.

- The number of firms engaged in trade reached 618,000, including over 540,000 private enterprises. Private firms accounted for 6.78 trillion yuan in trade, up 16.2 percent year-on-year and raising their share to 57.3 percent of total trade. Foreign-invested enterprises recorded 3.47 trillion yuan in trade, up 16.1 percent from a year ago and marking eight consecutive quarters of growth.

- China’s export structure shifted towards innovation and high-quality sectors, while import momentum strengthened:

- Exports increased 11.9 percent year-on-year to 6.85 trillion yuan, with strong growth in green products such as 3D printers (up 119 percent), electric vehicles (up 77.5 percent), and lithium batteries (up 50.4 percent)

- Imports increased 19.6 percent year-on-year to 4.99 trillion yuan, a record high for the same period. Imports of electromechanical products and consumer goods rose by 21.7 percent and 5.4 percent respectively

Wang Jun, deputy head of the PRC’s General Administration of Customs, said at a State Council Information Office press conference that China’s first-quarter trade showed “strong momentum and a solid start.” He attributed the growth — which came against the backdrop of a complex and challenging external environment — to China’s “stable fundamentals, strong vitality, and robust drivers” in foreign trade.

Backdrop

The partial blockade of the Strait of Hormuz starting in March due to the outbreak of conflict in the Middle East has led to severe disruptions in global trade, shipping, and commodity flows, as well as sharp price increases.

Our take

The sharp “cliff-like” decline in China’s official export data in March, combined with an abnormal, non-consumption-driven surge in imports, exposes a significant gap between state propaganda and realities on the ground. The official data also reflects the structural strains facing China’s economy under the dual pressures of geopolitical tensions and weakening domestic demand.

1. PRC state media mostly downplayed the March trade data in promoting the official trade figures for the first quarter of 2026. Instead, state media emphasized cumulative quarterly totals and highlighted figures denominated in renminbi. These headline numbers were then interpreted as “evidence” of strong growth momentum at the outset of the 15th Five-Year Plan period.

However, the growth momentum narrative is challenged in viewing the March data on a standalone basis and when the figures are denominated in U.S. dollars. In March 2026, export growth in U.S. dollar terms rose by only 2.5 percent year-on-year, a sharp deceleration compared to the 39.6 percent surge in February. This is highly unusual under stable trade conditions. At the same time, China’s import costs rose significantly due to the U.S.-Iran war driving up energy and commodity prices. This saw China’s trade surplus nearly halved.

2. China’s export sector had served as a critical lifeline for the economy, particularly after three years of “zero-COVID” disruptions. The economic driver, however, showed clear signs of malfunction in March 2026. This reflects the structural impact of global supply chain reconfiguration and rising trade protectionism on China’s manufacturing base rather than short-term volatility.

i) China’s export growth to the United States plunged further to negative 26.5 percent in March 2026. This indicates that the structure of U.S.-China trade has undergone a fundamental reversal since President Donald Trump added new tariffs on China shortly after taking office for the second time in 2025.

For the full year 2025, China’s exports to the U.S. had already declined by 20 percent. Data from early 2026 indicates that this decoupling trend has not slowed despite a temporary “truce” in tariff tensions, but has instead accelerated.

ii) The sharp contraction in exports to the U.S. has directly impacted China’s labor-intensive industries. In 2025, exports of traditional products such as furniture, toys, and footwear to the U.S. fell by 6.1 percent to 12.7 percent. By March 2026, even products labeled as “high-tech” were unable to avoid targeted tariff pressures. This decline represents not only a loss of orders, but also the forced relocation or fragmentation of entire export-oriented industrial chains.

iii) For years, PRC official narratives portrayed ASEAN as a new growth engine for China’s foreign trade. Implicit in the narrative is the suggestion that China is reducing its reliance on Western markets. This narrative, however, was sharply contradicted by Beijing’s recent data. Export growth to ASEAN cratered, falling from 29.4 percent in the first two months of 2026 to just 6.9 percent in March.

The plunge in China’s exports to ASEAN countries is likely due to tighter U.S. restrictions. Much of China’s export surge to Southeast Asia has been driven by transshipment practices where ASEAN countries act as intermediaries to access U.S. and European markets. Channels for transshipment, however, are narrowing as the U.S. authorities strengthen rules-of-origin verification and expand anti-circumvention investigations (particularly targeting sectors such as solar and EV components in Southeast Asia).

Meanwhile, ASEAN markets and purchasing power are insufficient to absorb the excess capacity originally destined for Western markets. Once the re-export arbitrage diminishes, China–ASEAN trade will likely revert to a more fragile structure centered on raw materials and low-value intermediate goods.

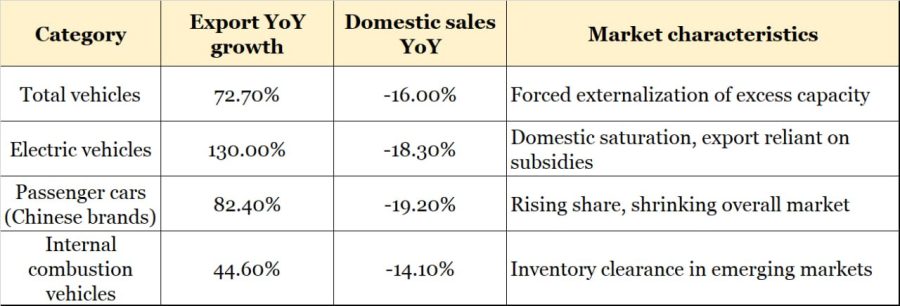

3. Official PRC narratives highlight a 72.7 percent surge in automobile exports as evidence of China’s manufacturing so-called “overtaking on the curve.” In reality, this surge is better understood as a disruptive overflow of excess capacity triggered by a collapsing domestic market.

In stark contrast to booming exports, China’s domestic auto market is experiencing a severe downturn. In March, domestic auto sales totaled only 2.024 million units, marking a 16 percent year-on-year decline. Domestic sales in the first quarter fell by 20.3 percent, reflecting the erosion of middle-class purchasing power amid vanishing real estate wealth effects and deteriorating employment expectations.

This “external boom, internal bust” dynamic points to a troubling trend: Chinese automakers are not expanding exports due to strong global demand, but because domestic competition has become unsustainable. Vehicles are being pushed into overseas markets at extremely low prices, and sometimes even at a loss. While officially framed as “trade resilience,” this is essentially a classic case of China exporting excess capacity.

Of the 875,000 vehicles exported in March, battery electric vehicle exports grew by 1.3 times, largely concentrated in lower-priced segments. This aggressive expansion is already triggering defensive trade measures globally. Countries and regions including Turkey, Brazil, the European Union, and North America have begun raising tariffs on Chinese EV imports to counter what is increasingly viewed as “deflationary export pressure.”

At the same time, official narratives obscure a sharp decline in profitability among exporters. Despite rising export volumes, higher shipping costs and intense price competition have eroded margins. Foreign exchange gains and operating profits have not kept pace with volume growth.

Beijing’s model of sacrificing profitability and international trade relations to sustain output amounts to a short-term fix with long-term risks. Should global tariff barriers continue to rise, Chinese firms’ reliance on exports to absorb excess capacity may face severe reverse shocks as external markets close.

4. Geopolitical instability triggered by Iran’s closure of the Strait of Hormuz in early 2026 cast an additional shadow over China’s foreign trade. As a critical chokepoint for global energy and chemical shipments, the disruption directly drove up shipping costs and insurance premiums. At a press conference on April 14, the General Administration of Customs was compelled to acknowledge that China’s trade with the Middle East had shifted from growth to contraction in March. More concerning, China’s trade surplus dropped sharply from $90.98 billion in February to $51.13 billion in March, and from $101.93 billion a year earlier to $51.13 billion. This indicates that the officially touted “trade resilience” is being undermined by real-world energy inflation.

This external shock has affected China’s trade on multiple fronts:

- Delivery cycles for exports have lengthened, while costs have surged.

- Rising energy import costs have further compressed the already thin margins of export-oriented firms. Although official narratives emphasize stable energy supply channels, the abnormal surge in March imports largely reflects high-priced procurements aimed at hedging geopolitical risks.

- Volatility in global energy, shipping, and commodity markets has indirectly weakened demand for Chinese exports in other Asian economies.

i) Against the backdrop of export growth slowing to just 2.5 percent, China’s imports (USD-denominated) surged by 27.8 percent in March. This far exceeded market expectations of 11.1 percent and marked a more-than-four-year high. However, this was not driven by stronger domestic consumption (retail sales grew only 2.8 percent in January–February), but rather by price effects.

The official March 2026 data reveals a severe divergence between import values and volumes:

- Copper ore: Import value +67%, volume +11.5%

- Fertilizers: Value +59%, volume +27%

- Integrated circuits (chips): Value +49%, volume +14%

This phenomenon of “paying more for less” reflects the global supply chain premium caused by Middle East tensions. As the world’s largest energy importer, China has been forced to absorb elevated “wartime premiums.”

Although China stockpiled crude oil at lower prices in January–February 2026, the outbreak of conflict in March pushed Brent crude to a one-year high, while LNG benchmark prices surged nearly 39 percent in a single day.

- Previously discounted Iranian oil (around 13 percent of imports) was disrupted due to infrastructure damage and shipping paralysis, forcing refiners into more expensive and competitive markets.

- Rising energy costs drove up input prices in southern industrial hubs such as Dongguan and Yiwu (e.g., plastics up around 40 percent), but weak global demand prevented firms from passing costs on to buyers. This compressed margins from both ends.

At the same time that import costs surged, the export engine stalled sharply in March, with growth falling from 21.8 percent in the first two months to 2.5 percent. This indicates that the conflict not only raised import costs but also undermined export capacity through shipping disruptions (notably via the Strait of Hormuz) and declining global purchasing power.

Taken together, the March 2026 trade data signals a sharp deterioration in China’s terms of trade. The shrinking surplus weakens support for the renminbi and exposes structural vulnerabilities in China’s energy security. Even with large strategic reserves, China remains unable to offset the fiscal and trade impact of systemic global commodity price increases.

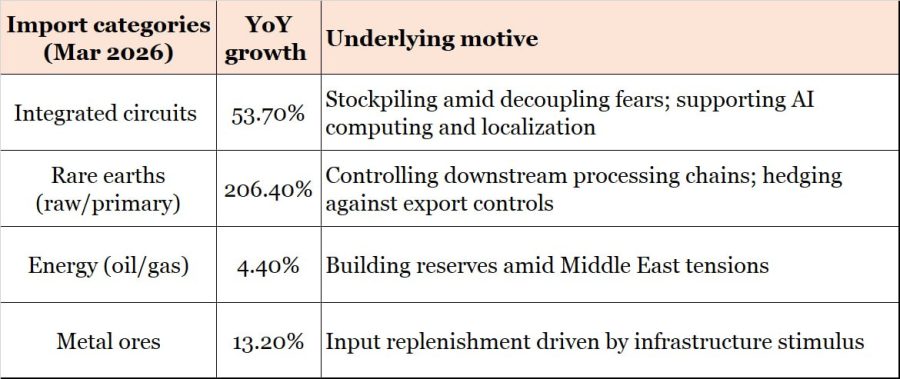

ii) Within China’s March import surge, unusually strong growth in high-tech goods and strategic materials stands out. In particular, imports of integrated circuits rose 53.7 percent while rare earth imports surged 206.4 percent.

China’s surge in chip imports is not driven by strong domestic end-demand for electronics, but by deep concerns over technological decoupling. Chinese firms appear to be aggressively stockpiling mature-node components to sustain production in key sectors in anticipation of potential future tightening of U.S. restrictions on advanced chips and manufacturing equipment.

The spike in rare earth imports reflects a geopolitical strategy rather than market dynamics. On one hand, China imposed two rounds of export controls in 2025 to exert leverage over global high-tech industries. On the other, it is leveraging its dominant processing capacity to absorb raw materials from Southeast Asia and Africa, preventing alternative supply chains from emerging.

China’s consumer goods imports in March remain weak once strategic and infrastructure-related imports are excluded. Although the official data lists a 5.4 percent increase in consumer goods imports in the first quarter of 2026, this is largely attributable to one-off demand during the Chinese New Year period. In routine March trade flows, household demand for imported goods appears stagnant.

The combination of weak exports and surging imports — driven by security-oriented spending — suggests a shift from an “export-for-earnings” model toward “spending-for-security.” This poses pressure on both the renminbi and fiscal balance in the long run.

5. While Official PRC narratives have been spotlighting the “new three” (electric vehicles, lithium batteries, and solar cells) industries, traditional pillars such as steel and basic manufacturing are exhibiting clear signs of distress.

Data shows that China’s steel exports fell 10 percent in Q1 2026, with March exports down 12.6 percent year-on-year to 9.14 million tons. This reflects a loss of competitiveness in global markets due to elevated input costs and rising trade barriers. More fundamentally, the reduced internal demand for steel in China is linked to the collapse of the domestic real estate sector.

Previously, China’s excess steel capacity could be absorbed through exports. But this outlet is now increasingly constrained as countries (including India and Southeast Asian economies) implement anti-dumping measures. The decline in steel exports also signals the exhaustion of China’s infrastructure-driven growth model.

At the same time, metal ore imports rose 13.2 percent in March, creating a striking contradiction amid falling steel exports. This highlights the “double squeeze” facing heavy industry:

- Upstream: Persistently high raw material costs due to global inflation and geopolitical tensions.

- Downstream: Weakening demand and falling prices for finished goods.

This widening margin squeeze is rapidly eroding corporate balance sheets and foreshadows a new wave of large-scale industrial bankruptcies.

6. In reporting the Q1 2026 data, PRC state media adopted a familiar “highlight the positives, omit the negatives” (報喜不報憂) approach. Outlets such as the People’s Daily and Xinhua heavily touted China’s “robust consumer market” and “innovation vitality,” using tourism data from the New Year and Chinese New Year holidays to obscure the economic slowdown evident in March.

Official claims point to a 31.2 percent increase in AI-related patent authorizations and a 45.5 percent rise in investment in strategic emerging industries. At the micro level, however, much of this investment is driven by government-guided funds and state-owned enterprises fulfilling political mandates rather than organic, market-based R&D demand.

The official March export data shows that although integrated circuit exports grew by 84.5 percent, their share in total exports remains insufficient to offset the sharp decline in exports to the United States (negative 26.5 percent) and the contraction in traditional sectors such as steel. This pattern of “localized prosperity amid overall deterioration” is repackaged as “structural optimization.” In fact, high-tech industries have significantly lower employment absorption capacity than traditional manufacturing. The resulting “employment gap” during this transition is contributing to rising youth unemployment, which Beijing then statistically masked with the category of so-called “flexible employment.”

The issuance of special-purpose local government bonds rose 20.8 percent year-on-year in Q1, primarily directed toward computing infrastructure and major projects. This helps explain the relatively strong performance of raw material and equipment imports. In essence, authorities are attempting to sustain headline GDP growth — targeted at 4.5%–5% — through debt expansion.

However, such debt-driven “forced starts” do not translate into export competitiveness. The new export orders index in March 2026 remained below the 50 percent expansion–contraction threshold, indicating persistent skepticism among global purchasing managers toward long-term demand for Chinese goods. This reliance on debt to “decorate” economic data risks further weakening local government balance sheets and embedding deeper financial vulnerabilities.

7. A key second-order effect visible in Beijing’s March 2026 export data is the consequence of China’s strategy to control critical minerals. The rare earth export controls implemented in 2025 began to show adverse effects in March 2026, with exports of rare earth-related minerals plunging 27.5 percent. What was intended as leverage against U.S. tariffs appears to have instead accelerated global diversification away from China.

A report by the European Central Bank indicates that 80 percent of large European firms have begun seeking alternative sources or reducing dependence on China’s processing chains. This “weaponization of trade” is eroding China’s long-established dominance in global supply chains. The contraction in March exports suggests a potential future scenario in which China faces isolation in high-tech materials markets and where it holds inventory without sufficient demand.

To offset the negative impact of its own export controls, China sharply increased imports of rare earth raw materials in March (up 206.4 percent). Beijing’s strategy appears to be the maintenance of influence by controlling processing nodes even as export volumes decline. This, however, represents a high-cost, low-efficiency defensive posture. As countries such as the United States, Australia, and Vietnam develop independent refining and processing capacity, China’s ability to exert leverage through monopoly control will rapidly diminish.

8. China’s official March 2026 trade data reveals three high-risk trends:

i) China’s exports no longer face pressure solely from the United States. As Chinese companies expand the dumping-like exports of vehicles and industrial goods, multiple markets (Brazil, India, the European Union, ASEAN, etc.) are likely to form a coordinated defensive response in the second half of 2026. If so, the growth model (relying on low prices to capture market share) that brought China its “robust” Q1 growth will become unsustainable and is likely to malfunction.

ii) The March import surge is concentrated in production inputs and strategic materials, while consumer goods imports remain weak. This indicates an intensifying deflationary cycle domestically.

As export-oriented firms face declining orders and are forced to cut wages or lay off workers, domestic consumption will weaken further, creating a negative feedback loop:

falling demand → excess capacity → export dumping → trade retaliation → corporate failures

iii) The stark divergence between March standalone data and Q1 aggregate figures is likely to further undermine international confidence in China’s statistics. Discrepancies between data from the foreign exchange regulator and customs — particularly in services versus goods trade balances — suggest that capital outflows are accelerating through trade channels. This underlying capital flight represents a far more critical concern than the official data narrative suggests.

9. All in all, the sharp fluctuations in China’s March 2026 trade data are not the result of “seasonal adjustments” or “short-term volatility,” as officially claimed. Rather, they signal a structural turning point, or the end of an era in which China relied on globalization dividends and export expansion to offset domestic imbalances.

The seemingly strong Q1 growth is largely a statistical artifact driven by base effects, front-loaded orders under geopolitical pressure, and panic stockpiling amid technological containment. By contrast, the March 2026 figures (2.5 percent export growth, negative 26.5 percent exports to the U.S., and negative 27.5 percent rare earth exports) offer a more accurate reading of economic conditions.

Beijing’s attempts at reframing the narrative through concepts such as “new-quality productive forces” do little to change underlying realities. China faces weak rule-of-law protections, declining private sector confidence, and a deteriorating global trade environment. These systemic weaknesses will be hard to offset by the “new growth drivers” alone.

China’s economy appears to be entering a prolonged and painful adjustment phase, with Q1 2026 representing the final afterglow before the illusion of resilience fades. Professional investors and international observers should recognize that China’s apparent “strong start” to the year in trade rests on fragile statistical presentations. Data from the second and third quarters will more accurately reflect the combined impact of rising global tariff barriers and collapsing domestic demand on China’s trade.

Optimism based solely on official data carries substantial political and economic risk. China is transitioning from a primary engine of global growth to a major source of excess capacity within the global trading system, and one of which the spillover effects are only just beginning to unfold.