1 The PBoC’s new interest rate policy: profit concession or risk management?

PBoC issues draft regulations on interest rates

On June 5, the People’s Bank of China announced that it plans to “further deepen interest rate market-oriented reforms.” To that end, the central bank is revising its regulations on renminbi interest rate administration (人民幣利率管理規定) to regulations on RMB deposit and loan interest rate administration (人民幣存貸款利率管理規定), and is now soliciting public comments on a draft.

The draft regulations are based on the original “Regulations on RMB Interest Rate Administration (人民幣利率管理規定), which were formulated 27 years ago. The new framework consolidates various deposit and loan interest calculation and settlement rules that are currently scattered across multiple departmental regulations and normative documents. It seeks to reshape the industry’s regulatory system from the perspectives of deposit and loan rate determination, interest calculation and settlement rules, and supervisory oversight.

According to the PBoC’s explanatory notes, the existing regulations were drafted and issued during an era of administratively controlled interest rates. Many provisions reflect a strong administrative-control approach, and some are no longer compatible with the direction of interest rate liberalization. Therefore, provisions involving administrative interest rate controls need to be revised.

The draft regulations consist of four chapters and twenty-nine articles. It specifies the scope of application, rules for interest calculation and settlement on deposits and loans, interest rate conversion formulas, and the responsibilities of the PBoC, its branches, and financial institutions. It also revises several provisions that have long drawn market attention, particularly penalty interest rules, which have been a major concern among market participants, and interest rate conversion and calculation formulas, which have generated numerous disputes.

Specifically, under the previous PBoC notice on issues concerning RMB loan interest rates (中國央行關於人民幣貸款利率有關問題的通知), overdue loans were subject to penalty interest rates of 30 percent to 50 percent above the contractual loan rate, while loans used for purposes inconsistent with the contract were subject to penalty rates of 50 percent to 100 percent above the contractual rate. The new draft replaces these fixed requirements with a market-based approach, allowing penalty rates, interest calculation methods, and grace periods to be negotiated between lenders and borrowers.

The draft regulations also redesign the pricing mechanism for medium- and long-term loans (with maturities exceeding one year, excluding personal mortgage loans). It allows lenders and borrowers to determine interest rates through commercial negotiations and permits adjustments on a monthly, quarterly, semi-annual, or annual basis during the contract term.

At the same time, the draft introduces a formal definition of improper deposit gathering practices, including offering excessively high deposit rates. Such practices include, but are not limited to, unauthorized manual interest supplements and offering rates that exceed the self-regulatory ceilings established under the market interest rate pricing mechanism, thereby disrupting fair competition in the deposit market.

In addition, the draft revises the rule in the “Notice on RMB Deposit and Loan Interest Calculation and Settlement Issues” (關於人民幣存貸款計結息問題的通知) that defined the daily interest rate as the annual rate divided by 360. Under the new proposal, the annual interest rate is calculated as the daily rate multiplied by 365 days (366 days in leap years), promoting a unified interest calculation standard for deposits and loans across financial institutions. The draft also adds provisions governing interest rate conversion and calculation formulas in cases involving compound interest.

Backdrop

The 1999 version of the “Regulations on RMB Interest Rate Administration” was created during an era of administrative interest rate controls, when the PBoC set benchmark rates and established permitted fluctuation bands for deposit and lending rates. Following the implementation of the Loan Prime Rate (LPR) reform in 2019, however, deposit and lending rates were largely liberalized, allowing financial institutions to price loans independently.

In recent years, intense competition among banks has led to severe “involution” within the sector. Loan rates fell rapidly, while deposit rates proved much more difficult to reduce. To compete for funding, commercial banks resorted to high-yield deposit products such as structured deposits, “smart deposits,” and manual interest supplements. The PBoC subsequently moved to regulate these practices.

Among these methods, “manual interest supplementation” was originally intended as a corrective tool for special interest-calculation requirements or operational errors. Under mounting pressure to attract deposits, however, it evolved into a mechanism for providing disguised interest subsidies. In some cases, corporate deposit rates exceeded loan rates, creating a distorted situation in which both deposits and loans expanded simultaneously despite weak underlying demand — a phenomenon often described as “low-rate lending, high-rate deposits, and dual balance-sheet expansion” (低貸高存、存貸雙增).

In April 2024, the PRC’s market interest rate pricing self-regulatory mechanism issued an initiative on prohibiting the use of manual interest supplements to attract deposits and maintaining orderly competition in the deposit market (關於禁止通過手工補息高息攬儲、維護存款市場競爭秩序的倡議). The initiative required banks to incorporate manual interest supplementation into monitoring systems and strictly prohibited practices such as pre-arranged interest guarantees or manual interest top-ups at maturity that effectively circumvented authorized deposit rate limits or self-regulatory ceilings. As a result, some artificially inflated deposits and loans were squeezed out of the banking system.

Previously, certain bank branches seeking to boost deposit volumes encouraged corporate clients to issue bills backed by pledged deposits or certificates of deposit. After discounting the bills, the proceeds would be redeposited, creating a circular process that inflated both deposits and loans. Companies could earn unusually high deposit returns through manual interest supplements and still retain arbitrage profits after accounting for discounting costs. Once manual interest supplementation was banned, this arbitrage chain was broken, causing corresponding declines in corporate deposit and loan balances.

Meanwhile, commercial banks’ net interest margins have finally begun to show signs of stabilization after sustained regulatory efforts to curb high-interest deposit solicitation and the repricing of maturing high-yield term deposits.

Our take

The PBoC has framed its revision of the decades-old RMB interest rate regulatory framework as a technical adjustment aimed at “deepening interest rate marketization reforms” and “improving the industry’s regulatory framework.” A closer examination of the legal provisions and current macro-financial indicators, however, suggests something else is afoot.

We believe that the central bank is responding defensively to a deep-seated structural debt crisis, and one that relies on a “long-acting anesthetic” rather than a “surgical intervention.” The move reflects the extent to which debt delinquency and rollover pressures within China’s financial system have approached a critical threshold, forcing policymakers to make institutional concessions.

1. The most significant change in the draft regulations on interest rates is the dismantling of the 27-year-old system of administratively mandated penalty-interest surcharges on overdue loans. The penalty-interest mechanism would shift from government-imposed pricing to negotiated arrangements between lenders and borrowers. This change suggests that Beijing’s assessment of the domestic debt situation has evolved from treating it as an acute emergency requiring temporary intervention after the COVID-19 pandemic to viewing it as a chronic condition that must be managed over the long term.

During the pandemic period between 2020 and 2022, the PBoC and financial regulators repeatedly issued temporary directives with strong administrative characteristics, requiring commercial banks to grant “phased extensions of principal and interest repayments” to small businesses and designated groups. These emergency measures all contained explicit expiration dates, creating periodic market anxiety whenever support programs approached their termination.

The current overhaul of the foundational regulations is fundamentally different. By embedding negotiable grace periods, flexible penalty-interest arrangements, and the possibility of repeated restructuring into the standard toolkit of commercial banking, Beijing is effectively transforming what were once extraordinary debt-relief measures into permanent institutional mechanisms governed by formal regulations. In effect, this represents an official acknowledgment that the balance-sheet damage suffered by many borrowers is not temporary but long-lasting. It grants frontline financial institutions a standing framework for regulatory protection, allowing banks to engage in legally compliant debt restructuring and loan rollovers as part of normal operations.

Such flexibility enables banks to provide relatively painless refinancing arrangements for entities such as local government financing vehicles (LGFVs), property projects included on official financing “white lists,” and individual mortgage borrowers facing repayment difficulties. The objective is to prevent rigid collection practices and escalating penalty-interest burdens from triggering broader waves of defaults that could threaten financial stability. Viewed from this perspective, the proposed reform is less about advancing market-oriented interest rate liberalization than about creating a durable institutional framework for managing and containing debt stress across the financial system. Rather than forcing rapid deleveraging, the revised rules would provide banks with greater discretion to extend, restructure, and refinance troubled debt, thereby reducing the risk of a disorderly unwinding of accumulated liabilities.

2. As the PRC is an authoritarian system, the PBoC’s proposed revision appears less like a routine financial reform and more like a form of crisis management. In such systems, the allocation of social resources is often driven not by principles of equal rights but by calculations of governance costs. When the extraction of private wealth approaches the limits of societal tolerance and begins to threaten fiscal sustainability or political stability, authorities may temporarily relax controls and offer limited concessions. Once the immediate crisis subsides, however, the underlying extractive logic frequently re-emerges in new administrative or technical forms. This historical cycle of “forced concessions followed by renewed extraction” can be observed in four prominent cases since the founding of the PRC.

Case 1: From “reform and opening-up” to the return of state dominance and the Golden Tax Phase IV System

After the end of the Cultural Revolution, the Chinese economy was on the verge of collapse as a result of centralized planning and extensive property expropriation. Fiscal deficits were severe, and the regime’s legitimacy was under pressure. To restore economic vitality, the CCP authorities loosened controls, allowing the household responsibility system in agriculture and tolerating the emergence of self-employed businesses and private enterprises. In practical terms, this temporarily returned a degree of economic autonomy and wealth-creation opportunities to ordinary citizens. However, as private wealth accumulated and digital surveillance technologies became increasingly sophisticated, the CCP authorities no longer viewed decentralized economic activity solely as an engine of growth. Instead, large private capital groups began to be perceived as potential challenges to political control.

Consequently, recent years have witnessed a renewed emphasis on state dominance in the economy. Major private-sector industries, including internet platforms, private tutoring companies, and property developers, have been subjected to extensive regulatory campaigns. At the same time, the nationwide rollout of the Golden Tax Phase IV system has expanded the state’s ability to conduct data-driven financial monitoring and tax enforcement. What began as a period of economic liberalization ultimately evolved into a new phase of state-led oversight and resource extraction through modern technological means.

Case 2: From the one-child policy to delayed retirement and pro-natal policies

Beginning in the 1980s, the CCP authorities implemented the one-child policy and enforced it through extensive administrative measures, including coercive birth-control practices and substantial fines for unauthorized births (commonly referred to as “social maintenance fees”). Over several decades, local governments collected large sums through these penalties while exercising extensive control over reproductive decisions.

The consequences of the one-child policy is China’s current demographic crisis, including a shrinking labor force, rapid population aging, and declining birth rates. These demographic trends pose long-term challenges to economic growth and the sustainability of pension systems. Belatedly, the CCP authorities abandoned the policy in recent years and are promoting larger families and pro-natalist policies.

The social maintenance fees collected under the one-child policy, however, were never refunded. Furthermore, as pro-natal policies have generated only limited results, CCP authorities have increasingly relied on delayed retirement reforms between 2024 and 2026. The burden created by earlier demographic policy failures is now being shifted onto workers through longer working lives and postponed pension eligibility.

Case 3: From land finance to mortgage rate cuts and consumer subsidies

Following housing reforms in 1998, local governments developed a highly dependent fiscal model based on land sales. Because governments maintained near-monopoly control over land supply, rising land prices translated into rising housing prices. Home purchases became a major financial burden for households, often requiring the combined resources of multiple generations.

After the property market downturn, major developers encountered severe financial distress, household wealth declined, and mortgage payment boycotts emerged in some areas. These developments posed risks not only to the real estate sector but also to the balance sheets of state-owned banks. In response, financial regulators introduced a series of supportive measures, including lower down-payment requirements, reductions in existing mortgage rates, and government-subsidized trade-in programs. These policies were not primarily intended as social welfare measures. Rather, they were designed to encourage households to continue deploying savings into the economy, thereby helping stabilize the banking system and preventing a real-estate downturn from escalating into a broader financial crisis.

Case 4: From dual-track social welfare systems to reductions in individual medical accounts

The PRC has long operated a dual-track welfare system in which public-sector employees generally receive more generous pension and healthcare benefits than workers outside the state sector. While private-sector employees and farmers contribute substantial premiums, they often receive comparatively limited benefits.

The fiscal strain generated by the three-year “dynamic zero-COVID” policy placed significant pressure on local government finances and medical insurance funds. In response, the CCP authorities promoted reforms that were officially presented as efforts to increase fiscal support for public healthcare insurance. However, the practical effect of these reforms was to reduce allocations to individual medical savings accounts and transfer more funds into pooled government-managed insurance funds. These changes sparked protests among some retirees, who viewed the reforms as a reduction in benefits that had previously been regarded as personal assets. When fiscal resources become strained, the system’s response is not necessarily to reduce benefits enjoyed by politically connected groups but rather to redirect resources from the broader population into centrally managed funding pools.

The central bank’s proposed revisions to previous regulations on interest rate management appear to be a “concession” of profits. But in essence, the policy is much like the four typical cases mentioned above — merely a crisis management tool used when the CCP regime faces a crisis.

3. The PBoC’s decision to revise the interest rates regulations could also be influenced by the macroeconomic and financial-sector data of the past two years. If the problem were merely a handful of isolated corporate defaults, the central bank would have little reason to overhaul a decades-old regulatory framework and introduce measures that effectively grant borrowers greater flexibility. Instead, the evidence suggests that the financial system as a whole is facing a period of severe internal strain, characterized by weakening profitability and deteriorating asset quality.

i) Data released by the National Financial Regulatory Administration indicate that both the liability side and profit-generating capacity of the banking sector are under mounting pressure.

After remaining flat at 1.42 percent for three consecutive quarters in 2025, the overall net interest margin (NIM) of commercial banks resumed its decline in the first quarter of 2026, falling to a record low of 1.40 percent. Among the large state-owned commercial banks, net interest margins reportedly declined even further, reaching approximately 1.29 percent, a level viewed by many analysts as approaching a danger zone. A 1.40 percent NIM is significantly below the widely recognized 1.80 percent threshold generally considered necessary for healthy banking operations.

As a result of sustained margin compression and policies requiring banks to support the real economy through lower lending rates, commercial banks generated cumulative net profits of 632.3 billion yuan in the first quarter of 2026, representing a year-on-year decline of 3.73 percent. Profit growth therefore shifted from positive growth of 2.3 percent for the whole of 2025 into outright contraction. This suggests that the banking sector is increasingly losing its ability to replenish capital through retained earnings, a classic sign of internal capital-generation weakness and balance-sheet deterioration.

ii) Official statistics show that China’s commercial banking sector’s non-performing loan (NPL) ratio increased only marginally to 1.51 percent at the end of the first quarter. However, data from China’s market for the transfer of retail non-performing assets suggest that underlying credit stress may be significantly greater than headline figures imply.

According to statistics from the Banking Credit Asset Registration and Transfer Center (Yindeng Center), more than 245 retail NPL packages were listed for transfer during the first quarter of 2026 (excluding relisted packages), involving over 39.9 billion yuan in outstanding principal and a combined principal-and-interest value exceeding 53.7 billion yuan. March alone accounted for 185 listed projects, representing around 25.6 billion yuan in principal, a 35 percent increase from the same period in 2025.

Particularly noteworthy was the surge in non-performing consumer finance loans. During the first quarter, eighteen consumer finance companies issued fifty-four new transfer announcements involving retail NPL portfolios with outstanding principal totaling 21.5 billion yuan. The volume of principal transfers increased by 141 percent year-on-year, making consumer finance companies one of the fastest-growing suppliers of distressed assets in the secondary market. Consumer loan NPL portfolios accounted for about 71 percent of the total listed principal volume, becoming the dominant category in the market, while the share represented by credit-card-related bad debts declined noticeably.

Another notable trend was the shortening of delinquency periods. The average overdue age of asset packages in the first quarter fell to 690 days, a decline of 22 percent from the previous quarter. Roughly 40 percent of the asset packages contained loans that had been delinquent for less than 300 days.

Based on these figures, one can reasonably infer that an increasing number of financial institutions are adopting an “early-transfer, rapid-disposal” strategy, seeking to sell distressed assets shortly after delinquency occurs rather than waiting for lengthy recovery efforts. The rationale is straightforward: early disposal reduces compliance costs, collection expenses, staffing burdens, and regulatory risks. This collective shift toward rapid asset disposal may also indicate a highly pessimistic internal assessment of borrowers’ future repayment capacity.

iii) Against the backdrop of weakening internal capital formation, the central government has increasingly stepped forward to support the banking sector through targeted special treasury bond issuances.

- First Recapitalization Round (2025): The PRC Ministry of Finance issued 500 billion yuan in special treasury bonds, using the proceeds to inject capital into major state-owned banks including, the Bank of China, China Construction Bank, Bank of Communications, and the Postal Savings Bank of China. The objective was to strengthen their Common Equity Tier 1 (CET1) capital positions, which had come under pressure from policies requiring banks to provide support to the real economy.

- Second Recapitalization Round (2026): On May 22, 2026, the first tranche of 300 billion yuan in special treasury bonds designated for capital injections into central financial institutions was formally issued. The bonds were split into five-year and seven-year maturities. Market participants generally expect the proceeds to be directed toward the two remaining major state-owned banks, namely, the Industrial and Commercial Bank of China and Agricultural Bank of China.

Taken together, these two rounds of recapitalization amount to 800 billion yuan and effectively establish a systemic capital support framework covering all major state-owned commercial banks. If pressures arising from local government debt restructuring, debt rollovers, and extensions granted to property sector “white-list” projects were not approaching levels capable of materially eroding bank capital, it is unlikely that the central government would deploy such a substantial amount of sovereign credit resources within a two-year period to reinforce the banking sector.

4. Another possible factor behind the PBoC’s decision to revise the long-standing regulations is the widespread deterioration of underlying financial assets in recent years and the growing number of local small and medium-sized financial institutions facing technical insolvency. Although official narratives have characterized the ongoing consolidation of small and medium-sized banks as a campaign to “reduce risks through reform” and “improve quality through consolidation,” this is, in reality, a large-scale hidden liquidation in which troubled institutions disappear without formally declaring bankruptcy.

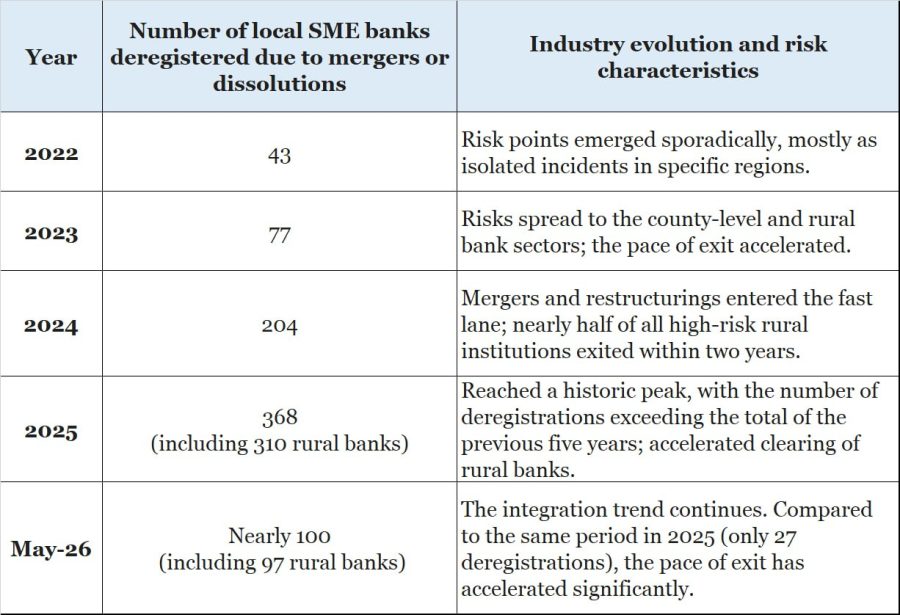

According to financial license records released by the National Financial Regulatory Administration and data compiled by Enterprise Early Warning Information services, the number of local banking institutions whose licenses have been revoked following regulatory-approved mergers or dissolutions has increased dramatically.

From May 2024 to early 2026, more than 400 local small and medium-sized banking entities reportedly had their financial licenses canceled within less than two years. This stands in stark contrast to the historical norm, when only a handful of institutions exited the market each year.

To prevent public concern over the health of smaller banks from developing into a broader loss of depositor confidence and potential bank runs, policymakers have largely relied on two administrative approaches to absorb and conceal financial risks:

i) The “village bank-to-branch” merger model:

The first and increasingly dominant approach involves transforming village and township banks into branches or subsidiaries of larger institutions. Under this model, the independent legal status of a village bank is terminated, while its assets, liabilities, branch network, and employees are absorbed by its sponsoring bank. The original institution typically continues operating at the same location but under the name of the acquiring bank.

For example, on May 28, 2026, Shengjing Bank announced the absorption of four affiliated Fumin village banks located in Xinmin, Shenbei, Faku, and Liaozhong, resulting in the cancellation of their financial licenses. Similarly, on May 29, 2026, Shanghai Rural Commercial Bank oversaw the merger of several village banks in Yunnan Province — including institutions in Kaiyuan, Gejiu, Jianshui, and Mile — into its sponsored Mengzi rural bank, with the acquired entities subsequently converted into branches.

ii) Provincial rural commercial bank consolidation:

The second approach involves the large-scale integration of county-level rural credit cooperatives and rural commercial banks whose ownership structures are often fragmented and whose balance sheets may contain significant problem assets. Under this model, provincial governments and state-owned asset authorities coordinate the issuance of special bonds dedicated to supporting smaller banks. The proceeds are then used to create unified provincial rural commercial banking groups operating under a single legal entity.

During 2025, two provincial rural credit union systems and four rural cooperative banks reportedly completed their exits through such restructuring programs. In March 2026, the Gansu Provincial Rural Commercial Bank Union also formally completed its deregistration as part of this broader consolidation effort.

The widespread trend of large banks absorbing smaller institutions and provincial governments injecting capital is not primarily a market-driven process. Rather, it serves as a mechanism through which larger financial institutions, with stronger balance sheets, larger asset bases, and greater earnings capacity, are used to absorb, dilute, and manage the bad debts accumulated by weaker local banks. The objective is to maintain the appearance of stability and avoid the politically sensitive outcome of publicly acknowledging bank failures. Therefore, the ongoing consolidation wave effectively transfers the costs of resolving local banking-sector problems into broader pools of financial resources, including the balance sheets of larger banks and, ultimately, the creditworthiness of the state itself. What is officially presented as a program of risk reduction and institutional optimization can also be viewed as a large-scale effort to contain the legacy consequences of decades of aggressive local financial expansion, poor credit allocation, and accumulated non-performing assets while preserving confidence in the banking system.

5. Another likely key objective of the PBoC’s revised deposit and lending rate regulations is to crack down on high-interest deposit solicitation by completely shutting off practices such as “manual interest supplementation” and “deposit-loan linkage” at the regulatory level. This policy package directly targets the extensive financial arbitrage ecosystem that has developed within China’s banking sector in recent years.

Before the release of the new regulations, lending rates fell rapidly under the guidance of the loan prime rate mechanism, while deposit rates declined much more slowly as banks aggressively competed for deposit growth. This created a distorted environment of “low-cost borrowing and high-yield deposits.” Large state-owned enterprises and other entities benefiting from policy support could leverage their strong credit profiles to obtain policy-driven loans from major banks at exceptionally low rates, sometimes around 2.5 percent, under programs intended to support the real economy.

Rather than being invested in productive activities, however, some of these funds were reportedly redeposited into banks offering elevated deposit returns. Through practices such as manual interest supplementation — where banks provided additional returns outside normal interest-calculation systems under various administrative labels such as consulting fees or service fees — depositors could receive effective yields exceeding 3.2 percent. Under this arrangement, borrowers could earn a risk-free spread simply by holding deposits. As a result, funds circulated within the financial system itself rather than flowing into productive investment, creating a structural contradiction characterized by rapid monetary growth, expanding credit aggregates, and weak real-economy activity.

To break this arbitrage chain, the new regulations not only prohibit manual interest supplementation but also comprehensively revise interest-rate conversion standards and interest-calculation formulas, areas that have historically generated significant disputes. One notable change is the abolition of the long-standing convention under the “Notice on RMB Deposit and Loan Interest Calculation and Settlement Issues” that defined the daily interest rate as the annual rate divided by 360 days. The new framework adopts a calculation based on the actual number of days in a calendar year, defining the annual rate as the daily rate multiplied by 365 days (or 366 days in leap years). In addition, the regulations introduce new provisions governing interest-rate conversion and calculation methods in situations involving compound interest.

At first glance, changing the calculation basis from a 360-day year to an actual 365- or 366-day year may appear to be a minor technical adjustment. However, the move substantially reduces opportunities for financial institutions to exploit accounting-day conventions in order to provide hidden interest subsidies or engage in interest-rate arbitrage. Once high-interest deposit solicitation and manual interest supplementation are explicitly prohibited and subject to regulatory penalties, the profitability of the “borrow low, deposit high” strategy is significantly diminished. Consequently, idle corporate funds and unused credit lines may be pushed toward more substantive uses, such as debt repayment or productive investment.

6. The draft regulations may objectively help reduce the risk of a “hard landing” in the credit chain. However, this type of flexible intervention — achieved by loosening financial rules and extending the effective timeline of default resolution — essentially uses liquidity-based measures to postpone a solvency problem. At the microeconomic level, such an approach inevitably carries significant financial and institutional costs.

As negotiated loan extensions and penalty-interest waivers become increasingly normalized, the composition of banks’ five-category loan classification system (Pass, Special Mention, Substandard, Doubtful, and Loss) is likely to undergo substantial structural changes. Many loans that would otherwise have been downgraded directly into the “substandard” or “doubtful” categories may instead be restructured through legally recognized extension agreements. Once repackaged into renewed contracts, these loans can, from an accounting perspective, remain outside the threshold of officially recognized NPLs.

As a result, the NPL ratio itself may become a less sensitive indicator of underlying credit conditions. The banking sector could increasingly display a pattern characterized by apparently stable asset quality on paper, rapid growth in special mention loans, elevated provisioning coverage ratios, and increasingly illiquid and inflexible underlying assets. Under such circumstances, a significant portion of actual credit risk may migrate into the “special mention” category, which effectively serves as a holding reservoir for potentially troubled loans. In this view, risks are not eliminated but merely shifted and concentrated within a growing pool of loans that have not yet been formally classified as non-performing.

Concurrently, the broad discretion granted under the new framework regarding penalty-interest arrangements could create substantial room for informal operational practices within financial institutions. Under China’s system of lifetime accountability for lending decisions, local bank managers and lending officers often face strong incentives to avoid recognizing problem loans during their tenure. Critics argue that the new rules could potentially enable some institutions to repeatedly renegotiate contracts, waive penalty interest, and extend grace periods, thereby keeping fundamentally distressed loans classified as restructured or “special mention” assets rather than recognizing them as bad debts.

From this perspective, the immediate benefit of reducing short-term default pressures may come at the cost of accumulating longer-term credit risks. Rather than resolving impaired assets outright, continual restructuring could defer loss recognition and transfer responsibility into the future. Consequently, what appears to be a stabilization mechanism in the short run could increase the risk that unresolved credit problems gradually accumulate beneath the surface of the banking system. The outcome would be a financial landscape in which reported indicators remain relatively stable, while underlying asset quality deteriorates more slowly and less visibly, creating the potential for larger credit challenges to emerge at a later stage.

7. Beijing’s most important strategy for coping with domestic balance-sheet deterioration is “delaying and waiting for change.”

The CCP leadership may believe that Western democratic systems have relatively low tolerance for financial crises and surging unemployment. When bad debts erupt or financial markets collapse, economic stress can quickly translate into political pressure. By contrast, Beijing possesses the administrative capacity to rewrite regulations, direct state-owned institutions to absorb losses, and deploy special sovereign bonds to stabilize the financial system. Under this logic, the strategic objective is not necessarily to resolve underlying structural problems immediately, but to delay their consequences through administrative intervention and financial support measures for five or even ten years. During that period, policymakers may hope that external developments — such as a U.S. debt crisis, renewed inflationary pressures in Western economies, or disruptive trade policies from a future U.S. administration — could weaken competing economies and alter the broader strategic balance. Time itself becomes a strategic asset.

However, many Western governments, led by the United States, are increasingly pursuing more proactive pressure strategies toward China.

One element of this pressure involves efforts to reduce China’s external revenue streams. Higher tariffs, stricter scrutiny of third-country transshipment arrangements, and broader trade restrictions are likely intended to reduce China’s export earnings and limit the inflow of foreign currency that has historically supported domestic investment and debt servicing. Constraining export-generated dollar earnings increases pressure on an economy already dealing with significant debt burdens.

A second area of pressure involves investment restrictions. The U.S. has expanded limitations on certain categories of American capital, including venture capital, private equity, and pension-fund investments, into selected Chinese technology sectors and strategic industries. These restrictions reduce China’s access to external capital and foreign-currency funding, forcing domestic financial institutions to shoulder a larger share of financing responsibilities. The burden increasingly falls on state-owned banks whose profitability has already been weakened by compressed interest margins.

Another concern relates to the expansion of financial sanctions. In 2026, the U.S. Treasury’s sanctions framework continued to target certain Russian financial institutions and related entities. Chinese financial institutions that conduct business with sanctioned entities face potential exposure to secondary-sanctions risks, including restrictions affecting access to the U.S. dollar financial system. Because access to dollar clearing infrastructure remains central to international finance, the threat of sanctions can have effects extending beyond the directly targeted institutions.

Beijing has historically sought to isolate sensitive cross-border transactions and higher-risk activities from major state-owned banks by allowing some business to be handled through smaller regional institutions. This arrangement can function as a financial firewall. However, if secondary sanctions were expanded to encompass these smaller institutions and their access to international dollar-clearing channels became restricted, the consequences could be severe. Many local and regional banks are already operating under significant balance-sheet pressure due to weak profitability, local-government debt exposure, and property-sector risks. Under such circumstances, external financial restrictions could accelerate liquidity stress and force authorities to move more quickly than planned in restructuring or consolidating troubled institutions. As a result, a gradual strategy of absorbing and merging weaker banks over time could potentially become a much more urgent process of crisis management.

In the past, Beijing has reportedly tended to route sensitive capital flows and certain cross-border settlement activities involving Russia and the Middle East through smaller local and regional banks, seeking to create a financial firewall that insulated major institutions from potential external risks. Should Western governments impose secondary sanctions on these smaller banks and restrict their access to U.S. dollar settlement channels, local financial institutions that are already operating near the threshold of what critics describe as “technical insolvency” could experience an immediate liquidity squeeze. Such a development would likely disrupt Beijing’s preferred strategy of gradually and quietly consolidating smaller banks in order to preserve financial and social stability. A process that had been designed as a slow-moving exercise in absorption and risk transfer could instead become an urgent effort focused on crisis containment, recapitalization, and loss management.

What had previously been a strategy of gradual concealment and controlled restructuring could be transformed into a much more acute process of financial stabilization under pressure. Sino-U.S. competition has increasingly evolved into a contest between two different forms of economic pressure. On one side, Western governments seek to apply external constraints through trade restrictions, capital controls, financial sanctions, and pressure on external funding channels. On the other side, Beijing relies on centralized administrative coordination, state-directed financial support, regulatory flexibility, and fiscal resources to stabilize domestic institutions. The contest is already extending beyond trade and technology restrictions, and becoming a competition over fiscal capacity, institutional endurance, economic resilience, and the ability of each system to absorb and manage internal strains over time.

2 Decoding China’s new private equity regulations and underlying economic dilemmas

On June 5, the General Office of the State Council issued a guiding opinion on strengthening regulation, preventing risks, and promoting the high-quality development of private investment funds (關於加強監管防範風險促進私募投資基金高質量發展的指導意見; henceforth referred to as the “guiding opinion”).

The document serves as a top-level policy framework for China’s private fund industry, which manages assets totaling around 23 trillion yuan. Its central themes are “stronger regulation” and “risk prevention,” with the stated goal of addressing structural problems including incomplete market entry mechanisms, insufficient regulatory oversight, inadequate accountability among certain government and state-owned fund sponsors, and the use of some private funds as vehicles for illegal activities and concealed corruption.

The key provisions and policy priorities of the guiding opinion can be summarized into six major areas:

1. General requirements and regulatory principles

- Strictly prohibit private funds from engaging in disguised lending and “equity in form, debt in substance” (名股實債) structures.

- Adopt a differentiated supervisory approach under the principle of “one category, one policy.”]

- Emphasize regulation not only of lawful market participants but also proactive enforcement against unlawful activities.

2. Strengthening preventive controls at the source (tightening entry controls and local approval)

- County- and district-level governments are prohibited from establishing new government investment funds. Any new fund establishment must obtain approval from higher-level authorities. Where similar government funds already exist, no additional funds may be created; existing structures are encouraged to consolidate.

- Institutions seeking private fund registration and filing must first undergo joint assessment and consultation by local financial regulatory authorities and local offices of the securities regulator. Approval authority must not be delegated downward.

- Without authorization, no institution may use terms such as “private fund” or “venture capital fund” in its business name or business scope.

3. Comprehensive regulatory strengthening (full-cycle and look-through supervision)

- Promote revisions to the Securities Investment Fund Law. Introduce institutional arrangements to regulate private fund “gambling agreements” (valuation adjustment mechanisms).

- Refine risk assessment standards and crack down on practices such as hidden shareholding and channel-based structures.

- Establish a centralized private fund risk-monitoring platform to conduct look-through data analysis and improve risk-identification capabilities.

- Strengthen accountability for state-owned enterprises by tightening approval standards and preventing indiscriminate establishment of SOE-backed funds. Introduce incentive and evaluation mechanisms focused on long-term operational performance and policy effectiveness.

- Establish reporting channels and strengthen protection for whistleblowers.

- Intensify enforcement against illegal fundraising, embezzlement and misappropriation, self-financing arrangements, improper benefit transfers, illegal fundraising schemes, and unlawful cross-border capital movements. Major cases will be subject to coordinated inter-agency investigation and oversight.

4. Managing existing risks prudently (legacy cleanup and debt-control measures)

- Managers involved in serious violations, abnormal operations, long-term loss of contact, or failure to rectify problems will face deregistration or mandatory cancellation within prescribed time limits. Institutions using private-fund-related terminology without completing registration or filing procedures will face targeted rectification measures, mandatory relabeling, or license revocation.

- Local governments where institutions are registered will take primary responsibility for formulating risk-resolution plans, including asset recovery, financial cleanup, and capital verification. The authorities should aim to avoid creating expectations that public resources or the central government will automatically absorb losses.

- The policy explicitly prohibits the use of private funds to engage in unauthorized borrowing, debt restructuring, or the disposal of distressed enterprises in ways that generate new systemic risks.

5. Promoting standardized development (building “patient capital”)

- Strengthen internal controls among fund managers. Establish blacklist systems and publicly disclose major violators, including institutions, investors, and practitioners.

- Expand funding channels for private equity and venture capital funds. Promote deeper integration between private capital and technological innovation.

- Prioritize investment strategies focused on early-stage companies, small enterprises, long-term capital deployment, hard-technology sectors, and mergers and acquisitions involving strategic emerging industries.

- Further standardize and improve diversified exit mechanisms. Implement differentiated regulatory approaches for venture capital funds.

6. Implementation and institutional support

- The China Securities Regulatory Commission (CSRC), together with relevant government agencies, will take responsibility for overall coordination and strengthening regulatory capacity.

Our take

The guiding opinion is the first public policy document on the private investment fund industry issued by the PRC State Council. The market has widely interpreted this as a “systemic upgrade” or policy overhaul on Beijing’s part.

The document presents itself as an effort to “support the strong, eliminate the weak, and separate genuine market participants from problematic ones,” and aims to guide China’s 23 trillion yuan private fund industry toward greater standardization through full-chain and look-through supervision. What Beijing is doing, however, likely extends beyond a conventional regulatory compliance campaign. The move appears to be a broader institutional response to mounting fiscal and financial pressures, shaped by the interaction between different governance legacies and the challenges facing China’s current economic model.

1. The liquidity shortages and exit difficulties currently affecting China’s private equity and venture capital markets are not simply the result of recent policy tightening. Rather, they are the cumulative outcome of financial structures that developed during earlier periods of rapid expansion and the current emphasis on stronger political oversight and centralized governance.

During the late 1990s and early 2000s, China’s private equity and venture capital sectors expanded quickly amid rapid economic growth and relatively decentralized local development incentives. In an environment where institutional safeguards and legal frameworks were still developing, some investment activities became closely intertwined with local political networks, preferential access to capital, pre-IPO investment opportunities, and value extraction through public-market listings. While this period helped create the foundations of China’s early capital markets and generated substantial wealth creation, it also contributed to governance weaknesses and incentives that prioritized financial engineering over long-term capital allocation.

Meanwhile, China’s 1994 tax-sharing reform created a structural imbalance in which fiscal resources became increasingly centralized while local governments retained broad spending and development responsibilities. To sustain GDP growth and meet performance targets, local authorities increasingly relied on financing vehicles, regional financial institutions, and eventually government-guided investment funds as mechanisms for funding development and attracting investment. This model allowed local governments to expand financing outside traditional budget constraints while simultaneously increasing hidden liabilities and weakening transparency.

Facing these accumulated financial and governance challenges, the Xi Jinping leadership has adopted a governance approach centered on stronger Party leadership and greater central coordination. In recent years, CCP authorities have imposed tighter oversight across multiple sectors, including internet platforms, education services, and real estate. Officially, these policies have been framed as efforts to prevent what regulators describe as the “disorderly expansion of capital.” However, the pace and intensity of intervention contributed to increased uncertainty regarding regulatory predictability and investment confidence, encouraging more cautious behavior among domestic investors and contributing to weaker foreign direct investment flows.

Within the administrative system itself, anti-corruption campaigns combined with stricter accountability mechanisms have also altered bureaucratic incentives. These pressures have encouraged a more risk-averse administrative culture, where avoiding errors may become more important than pursuing innovation or taking initiative. In finance and state-asset management, this environment has reinforced a preference for minimizing perceived losses of state assets even when doing so constrains private-sector activity.

At the same time, regulators have periodically tightened or slowed initial public offering approvals in order to stabilize China’s domestic equity markets. For private funds, IPO access represents a crucial exit channel and an essential component of the investment cycle — raising capital, investing, managing assets, and ultimately exiting investments. When exit channels become constrained, capital recycling slows significantly.

2. The State Council’s introduction of the guiding opinion at this time reflects growing concerns within the CCP across three areas: the structure of capital formation, local governments’ attempts at financial self-rescue, and the protection of state-owned assets.

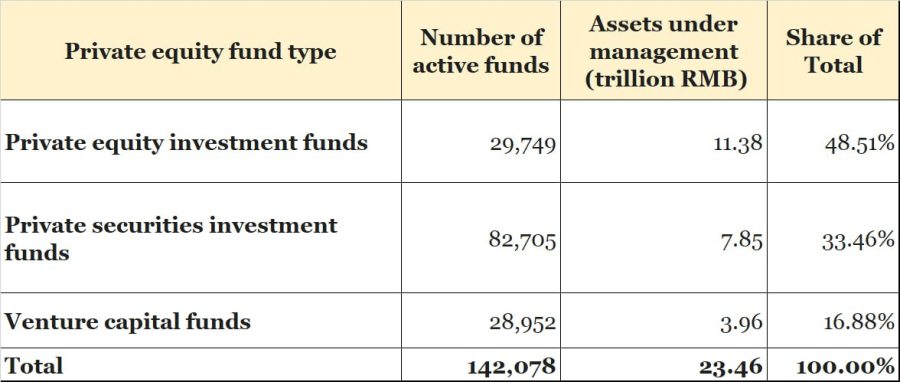

i) According to the latest statistics released by the Asset Management Association of China (AMAC), China’s outstanding private fund industry reached around 23.46 trillion yuan at the end of April 2026. This headline figure conceals a growing structural imbalance increasingly characterized by bureaucratic concentration.

The data above suggests that in private equity and venture capital — the dominant segments of China’s primary capital market — the composition of new fundraising has become heavily skewed. Market estimates indicate that state-backed capital and local government guidance funds (state-owned LPs) now account for roughly 70 to 80 percent of newly raised capital in the primary market. By the first quarter of 2026, managers with state-linked backgrounds reportedly represented 35.7 percent of the market, while the share of state-controlled fund managers increased from 11.6 percent a decade ago to 32.5 percent. This indicates that the primary market has increasingly lost access to private and foreign capital and has gradually evolved into an internal cycle in which: government borrowing → government guidance funds → state-backed managers → local SOEs or designated projects. This structure risks weakening market efficiency and reducing the role of independent capital allocation.

ii) Local governments have faced widening funding gaps with the prolonged weakness in the property market and the decline of land-sale revenue. Beginning in 2024, the central authorities intensified efforts to standardize and eliminate local preferential tax and fiscal incentives, reducing traditional methods used to attract investment. As a result, many local governments increasingly shifted toward “fund-based investment promotion” using local state-owned investment platforms and guidance funds to attract projects through equity investment.

When pursued without sufficient professional evaluation capacity, this model can create substantial financial and governance risks. One frequently cited example emerged in April 2026, when the disciplinary authorities publicly reported a case involving investment losses by state-owned capital in Xinyu, Jiangxi Province. According to official disclosures, in 2020 the local government investment platform acquired control of the listed company Qixin Co. for approximately 1.094 billion yuan as part of efforts to achieve local listing targets.

Subsequent investigations found that the company had engaged in financial misstatements for about eight years prior to the acquisition. Between 2012 and 2019, the company allegedly overstated revenue by 1.31 billion yuan and inflated profits by 2.63 billion yuan. After local state-owned capital became involved, the local authorities reportedly continued extending substantial loans to the company in an effort to stabilize operations and prevent the investment from collapsing. Despite these efforts, the company was ultimately delisted on July 5, 2023. Before delisting, the residual value of Xinyu’s equity holdings reportedly fell to only 28 million yuan, leaving most of the original 1.094 billion yuan investment effectively impaired. When subsequent loans and repayment obligations are included, total losses of state assets were reported at around 1.7 billion yuan. The case eventually resulted in the resignation of Xinyu’s mayor, while the chairman of the local government financing platform and other officials were detained or investigated on allegations including bribery and misconduct related to state-owned enterprise contract performance.

This kind of aggressive acquisition activity has contributed to a phenomenon that some Chinese financial commentators mockingly refer to as “beng lao tou” (崩老頭). Originally, the phrase referred to a colloquial social phenomenon in which younger individuals obtained modest financial benefits from older, financially secure partners through emotional companionship or ambiguous relationships — implying a situation where both parties willingly participated. More recently, the term has been repurposed as a satirical metaphor in financial commentary. In this newer usage, it describes situations in which local governments, under pressure to transform their economies and produce visible development outcomes, become vulnerable to ambitious pitches from private companies that package projects under labels such as “hard technology” or “new productive forces” in order to attract public capital and policy support.

Examples frequently discussed in public commentary include:

Dreame Technology

The smart cleaning and robotics company Dreame Technology (追覓科技) established a large number of off-balance-sheet platform entities and divided operations into more than 200 cross-functional business units, while promoting highly ambitious growth targets framed around a political-development narrative. The company claimed goals of reaching 300 billion yuan in output by 2027 and 1 trillion yuan by 2028.

Dreame Technology capitalized on local governments’ anxiety over economic transition and declining land-finance revenues, replicating what they describe as a “mass-production investment attraction” model. The company’s projects spanning air conditioners, recreational vehicles, industrial robotics, new energy vehicles, and other sectors were launched simultaneously across multiple jurisdictions — including parts of Jiangsu, Jiaxing in Zhejiang, Quanjiao in Anhui, Wuhan, and Taizhou in Zhejiang — through separate affiliated structures. This process enabled the company to obtain and redirect large volumes of local government guidance-fund capital and state-backed investment totaling hundreds of billions of renminbi.

In June 2026, financial media outlets published extensive reporting questioning Dreame Technology’s financing practices, describing them as excessively dependent on local fiscal resources. Subsequently, the company’s founder’s account on Weibo was reportedly restricted. Concurrently, fiscal and state-asset authorities across multiple provinces reportedly launched broad reviews, inspections, and post-investment assessments into the company, leaving parts of the project network facing severe operational and restructuring pressure.

Neta Auto

The electric vehicle startup Neta Auto has also been cited by critics as an example of investment risks associated with aggressive local government support. According to public reporting, the company accumulated net losses of approximately 18.3 billion yuan over three years, attributed to non-market operating practices, misjudgment of technology pathways, and price competition conducted despite negative gross margins.

Driven by competition to capture opportunities in the new energy vehicle sector, local governments — including Yichun (Jiangxi), Nanning (Guangxi), and Tongxiang (Zhejiang) — were described as engaging in increasingly aggressive investment attraction and subsidy programs involving Neta Auto. After the company halted production lines across multiple locations, it was featured in April 2026 by CCTV’s Focus Report as a negative example tied to local debt pressures and inefficient investment promotion.

As judicial restructuring proceedings progressed, Neta Auto’s total liabilities were reported to have reached 26.58 billion yuan, with concerns raised that more than 8 billion yuan in state-backed public capital invested across different localities could face substantial or total losses.

iii) Constraints in IPO exits have contributed to a buildup of illiquid holdings within China’s primary market. For managers overseeing state-backed capital, pressure from anti-corruption campaigns, auditing requirements, and long-term accountability mechanisms has increasingly shifted incentives toward procedural compliance.

When investment exit deadlines approach, some state-linked fund managers reportedly pursue legal enforcement of valuation adjustment agreements and share repurchase clauses. These actions are often interpreted not solely as commercial decisions but also as efforts to demonstrate compliance with obligations to preserve and increase the value of state assets.

Fund managers may recognize that startup companies affected by weak market conditions or delayed listings have limited ability to repay large buyback obligations. However, litigation itself can become an important procedural safeguard to document that managers fulfilled their responsibilities and did not allow losses to occur without formal action. This dynamic can place severe pressure on founders and private technology firms, particularly those operating in sectors such as semiconductors, biotechnology, and advanced manufacturing. Prolonged exit blockages combined with defensive legal behavior risk weakening entrepreneurial confidence, reducing risk-taking incentives, and placing additional strain on the broader innovation ecosystem.

3. In considering financial disorder at the local level and concerns over state-asset losses, the guiding opinion can be interpreted as a centralization and risk-control framework rather than a growth promotion policy.

Notably, the document places significant emphasis on centralizing authority and strengthening accountability mechanisms.

- The guiding opinion begins by strengthening controls at the point of market entry and establishing significantly tighter approval standards. One notable measure restricts financing activities at the county and district levels. This substantially reduces the ability of local governments to use investment funds as alternative financing channels or to conduct aggressive investment promotion outside formal fiscal frameworks. Naturally, financial decision-making authority increasingly shifts upward toward provincial and central authorities.

- The document introduces a dual-layer approval mechanism. Private fund institutions seeking registration and filing must first undergo a coordinated assessment process before they can apply for formal business registration. The criteria and procedures for this assessment are to be formulated centrally by securities regulators, and authority over approvals is explicitly not intended to be delegated downward.

- The guiding opinion prohibits financing structures commonly described as “equity in form, debt in substance,” along with tighter controls over the use of labels such as “private fund” and “venture capital fund.” These provisions appear to be an effort by the CCP authorities to standardize market behavior and improve transparency in an attempt to bring local financing activities and non-standard capital structures under tighter vertical supervision.

A second major feature of the policy framework involves reorganizing how financial risks are managed and assigning responsibility more explicitly.

- The document specifies that risks associated with private fund managers are to be handled jointly by provincial governments or centrally designated municipalities where the institution is registered, as well as national securities regulatory authorities and related agencies.

- For financial cases involving multiple jurisdictions or sectors, the central authorities plan to establish coordinated investigation and oversight mechanisms capable of tracing responsibility directly to local implementing bodies.

The institutional logic behind these arrangements is relatively clear. The central government is signaling that local investment funds and local financing decisions should increasingly remain the responsibility of the jurisdictions that create them. If future cases emerge involving major investment losses, debt problems, or state-asset impairment (such as controversial local investment projects listed above), local governments should not assume that losses will automatically be absorbed through central fiscal intervention. Instead, responsibility for financial outcomes and administrative consequences is intended to remain tied to local leadership and management decisions. This appears to be an effort by Beijing to engage in risk isolation and responsibility transfer (to the local authorities).

4. Beijing’s guiding opinion is intended to standardize the private fund market and promote the stated objective of “supporting stronger participants while eliminating weaker and non-genuine actors.” However, market forces may produce outcomes different from what policymakers intend.

The guiding opinion aims to strictly contain hidden local-government debt risks, curb indiscriminate investment, and prevent inefficient circulation of capital and unauthorized borrowing. Yet the broad suspension of new county- and district-level guidance funds could remove one of the few remaining policy tools available to less-developed regions for attracting investment and pursuing industrial upgrading. Grassroots fiscal conditions — particularly in central and western regions — may face further pressure, potentially reducing local governments’ ability to sustain economic development initiatives.

From a regulatory perspective, the guiding opinion seeks to eliminate what the central authorities describe as “pseudo-private funds” and irregular market participants while raising overall industry standards. However, comprehensive end-to-end supervision may also significantly increase compliance costs. In an environment shaped by anti-corruption enforcement and expanded accountability requirements, investment managers may increasingly perceive political and compliance risks as outweighing potential economic returns. This could encourage more defensive behavior, leading institutions to reduce fundraising and investment activity in order to minimize exposure. The policy could also lead to “regulatory paralysis” within parts of the private fund industry.

The guiding opinion aims to direct capital toward national strategic priorities and sectors associated with technological self-sufficiency and advanced industrial development. But if private and foreign capital continue to play a reduced role in pricing and capital allocation, investment decisions may become increasingly dependent on administrative priorities. A system dominated by state-directed capital may risk channeling resources toward projects that align well with policy targets rather than those with stronger commercial fundamentals. This dynamic could increase the likelihood of capital concentration in highly promoted sectors without generating corresponding economic returns.

The policy emphasizes improving diversified exit channels and standardizing valuation adjustment agreements in order to strengthen investor confidence. However, if administrative intervention in equity markets continues and IPO approvals remain constrained, exit bottlenecks will persist regardless of formal regulatory improvements. Without functioning exit channels, capital in the primary market becomes increasingly difficult to recycle. Therefore, administrative reforms aimed at improving exits may have limited practical effect unless accompanied by broader market reforms.

According to officially released first-quarter regulatory statistics, stronger supervision has coincided with substantial market exits. Reported figures included:

- 1,805 private fund managers and related entities were subject to administrative regulatory measures.

- 97 managers and related entities received administrative penalties.

- 86 suspected criminal cases were referred to public security authorities.

- 5,444 private fund manager registrations were canceled by the Asset Management Association of China.

The cancellation of 5,444 manager registrations within a single quarter represents an unusually large contraction by historical standards. While this could be interpreted as evidence of a successful cleanup and strengthening market discipline, such rapid consolidation also risks damaging market diversity and weakening the underlying ecosystem of the private capital market.

If private and foreign capital continue to retreat and state-backed capital becomes the dominant source of market pricing, systemic distortions may emerge.

- State-affiliated fund managers may increasingly evaluate projects based on factors such as policy alignment, local implementation outcomes, compliance risk, and preservation of state assets rather than purely commercial return or technological potential. This may incentivize highly visible, policy-oriented projects that excel at meeting administrative objectives.

- Companies focused on long-term basic research and deep-technology development, which often require patient capital and involve higher uncertainty, may find it more difficult to attract funding because they cannot guarantee immediate economic output, rapid localization, or near-term fiscal contributions. The challenge becomes balancing stronger regulatory discipline with maintaining enough market dynamism to support long-term innovation and capital formation.

5. The State Council’s guiding opinion is a reflection of China’s current economic governance model. It is also an attempt to revitalize the venture capital and private investment market — which are traditionally dependent on a high degree of openness, legal protection, intellectual property security, and market-based competition — through more rigid administrative controls and increasingly comprehensive regulation.

The financial distortions and structural imbalances that accumulated during the Jiang Zemin era (shaped by tolerated privilege networks and institutional loopholes created under the tax-sharing fiscal system) developed into deeper systemic problems over time. The Xi leadership has attempted to address these problems through an aggressive anti-corruption campaign, institutional cleanup, and regulatory tightening. While this approach may strengthen discipline and reduce certain forms of misconduct, it overlooks fundamental characteristics of market economies, namely, confidence and expectations. As long as three underlying conditions remain fundamentally unresolved — declining confidence among private enterprises, continued withdrawal of foreign capital, and IPO exit channels in the secondary market being constrained by stability-oriented policy considerations — this model of “full-chain strict regulation,” framed in the name of risk prevention but also serving the purposes of consolidating authority and reallocating responsibility, is unlikely to deliver the “high-quality development” emphasized in official policy narratives.

Stronger regulatory control alone cannot restore market vitality if the underlying drivers of investment confidence and capital circulation remain weak. Instead, the excessive emphasis on administrative oversight may produce a form of institutional self-constriction, reducing incentives for risk-taking, slowing capital formation, and weakening entrepreneurial activity. Such dynamics could accelerate contraction within China’s private equity and venture capital sectors and place additional pressure on local public finances and long-term innovation capacity. If regulatory tightening continues to outweigh improvements in capital mobility, market confidence, and exit mechanisms, China’s private equity and venture capital sectors may face prolonged contraction rather than renewal.