1 Beijing’s new real estate stabilization policies likely to have limited impact

Beijing unveils new real estate measures

Oct. 17

The PRC Ministry of Housing and Urban-Rural Development held a press conference along with the Ministry of Finance, Ministry of Natural Resources, People’s Bank of China, and the National Financial Regulatory Administration. The press conference announced a set of policy “combination punches” to stabilize the real estate market and arrest decline.

The policies include:

‘Four Cancellations’ (四個取消)

- Local governments are granted regulatory autonomy to implement property policies tailored to local conditions, including canceling restrictions on property purchases, sales, pricing, and the classification of ordinary and non-ordinary residential properties.

‘Four Reductions’ (四個降低)

- Lowering interest rate on housing provident fund loans.

- Reducing down payment ratios for housing loans. With the exception of Beijing, Shanghai, and Shenzhen, the vast majority of cities will no longer differentiate between first and second homes and the minimum down payment will be uniformly adjusted to 15 percent.

- Complete the reduction of interest rates on existing loans by Oct. 31, 2024.

- Reduce the tax burden for those selling old homes to buy new ones.

‘Two Increases’ (兩個增加)

- Implement the renovation of 1 million units in urban villages and dilapidated housing reconstruction through monetary measures.

- Increase financial support for real estate companies.

- Strive to include all qualified real estate projects in the “white list” by the end of the year. Ensure that all eligible projects are covered and receive loans to meet reasonable financing needs.

- Real estate projects on the “white list” have received approved loans amounting to 2.23 trillion yuan as of Oct. 16, 2024. Total credit scale for “white listed” projects will be increased to over 4 trillion yuan by the end of 2024.

The press conference also said that the National Financial Regulatory Administration will allow policy and commercial banks to issue acquisition loans for the purchase of idle land.

September real estate situation

Oct. 16

The Tianjin municipal government announced the complete removal of housing restrictions.

Chinese real estate stocks surged in the wake of the Tianjin authorities’ announcement, with the Shanghai Real Estate Index rising by 4.46 percent. However, the index fell by 6.01 percent the following day after the Ministry of Housing and Urban-Rural Development’s press conference.

Oct. 18

The National Bureau of Statistics released data on price changes for new and second-hand commercial residential properties in 70 key cities for September 2024.

New home prices

- The number of cities of the 70 where the sales prices of new homes decreased from a month ago and a year ago were 66 and 68 respectively (compared to 67 and 68 respectively in August).

- First-tier cities

- New home prices dropped 4.7 percent year-on-year (compared to a 4.2 percent decline in August) and decreased 0.5 percent month-on-month (compared to a 0.3 percent drop in August). September marked the 15th consecutive month of new home price declines.

- Year-on-year, new home prices in Beijing, Guangzhou, and Shenzhen fell by 4.6 percent, 10.3 percent, and 8.6 percent respectively, while prices in Shanghai rose by 4.9 percent.

- Month-on-month, new home prices in Beijing, Guangzhou, and Shenzhen fell by 0.7 percent, 0.9 percent, and 1.0 percent respectively, while prices in Shanghai increased by 0.6 percent.

- Second-tier cities

- New home prices fell by 5.7 percent year-on-year (compared to a 5.3 percent drop in August) and decreased 0.7 percent month-on-month (compared to a 0.7 percent decline in August).

- Third-tier cities

- New home prices fell 6.6 percent year-on-year (compared to a 6.2 percent drop in August) and dropped 0.7 percent month-on-month (compared to a 0.6 percent decline in August).

Second-hand home prices

- First-tier cities

- Second-hand home prices dropped 10.7 percent year-on-year (compared to a 9.4 percent decrease in August) and fell 1.2 percent month-on-month (compared to a 0.9 percent drop in August).

- Year-on-year, second-hand home prices in Beijing, Shanghai, Guangzhou, and Shenzhen fell by 10.3 percent, 7.6 percent, 12.8 percent, and 12 percent respectively.

- Month-on-month, second-hand home prices in Beijing, Shanghai, Guangzhou, and Shenzhen dropped by 1.3 percent, 1.2 percent, 1.1 percent, and 1.3 percent respectively.

- Second-tier cities

- Second-hand home prices fell 8.9 percent year-on-year (compared to an 8.6 percent drop in August) and declined 0.9 percent month-on-month (compared to a 0.8 percent drop in August.

- Third-tier cities

- Second-hand home prices dropped 9.0 percent year-on-year (compared to an 8.5 percent drop in August) and fell 0.9 percent month-on-month (compared to a 0.9 percent drop in August).

Our take

1. The September real estate data indicates that China’s property crisis has worsened. Beijing’s recent policies to stabilize housing prices also appear to be ineffective and have failed to address key issues plaguing the real estate sector.

The official real estate data for September is particularly bad considering that the CCP authorities typically “massage” the figures to make them look more favorable. For example, in first-tier cities where prices are traditionally more resilient, new home prices fell by 4.7 percent from a year ago and Guangzhou saw new home prices drop by 10.3 percent. Meanwhile, second-hand home prices declined by 10.7 percent from the previous year, with three of the four first-tier cities experiencing double-digit declines. Falling second-hand home prices reflect the declining financial appeal of real estate in China, and new homes are valuable only to fulfill essential housing needs because their value is bound to decline unless the property crisis is resolved.

The bleak real estate situation appears to be a key factor pushing Beijing to introduce more support policies and the localities to lift housing purchase restrictions.

2. We identified in the Oct. 3 newsletter that the nub of the real estate crisis was that many sold homes are unfinished projects, and not that inventory is unsold. Beijing’s latest real estate policies, however, miss the mark in addressing the critical issue. Of Beijing’s real estate market stabilization policies, the “Four Cancellations” and “Four Reductions” are geared towards easing restrictions on home purchases and reducing financing costs. Meanwhile, the “Two Increases” serve to increase housing supply, not move existing inventory.

Meanwhile, it is unclear how many real estate projects meet the “white list” criteria and are eligible to tap the 4 trillion yuan credit support. Real estate projects must meet regulatory requirements, and most unfinished projects are unlikely to qualify based on the 10 conditions listed by mainland media:

- All project permits must be completed.

- The project must not be undergoing bankruptcy restructuring.

- The project is not in a situation where it is being seized or frozen.

- The project must not have evaded financial debts.

- The project must not have committed any major legal or regulatory violations.

- The project must be under active construction, or at least capable of resuming construction promptly once funds are available.

- The developer must provide collateral matching the financing amount.

- The project must have a lead financing bank and a closed management system for loan funds.

- Pre-sale funds must not have been misappropriated or withdrawn pre-sale funds must have been returned. Project capital must also be fully in place and has not been withdrawn or misappropriated.

- A detailed plan for loan usage, project completion, and loan repayment must be in place.

Based on the conditions above, China Evergrande is unlikely to make it on the “white list” to secure funds to complete unfinished projects. Evergrande, however, is the developer with the most severe debt problems in the crisis. Meanwhile, developers that are able to provide collateral matching the financing amount would have already secured financing. Finally, many developers with unfinished projects on hand have likely misappropriated pre-sale funds, experienced sluggish sales, and are struggling with debts or defaults, making it difficult for them to enter the “white list” and access the extra financing that the CCP authorities are making available. We estimate that most of the projects that qualify for the “white list” are likely those belonging to state-owned real estate companies instead of large private developers.

It is also unclear whether the greater availability of loans will sufficiently address the unfinished building problem. The scale of the unfinished building problem is enormous. An International Monetary Fund proposal in August estimated that China would have to spend 5.5 percent of its GDP over four years, or almost $1 trillion, to complete and deliver pre-sold homes or compensate homebuyers. Bloomberg Intelligence also estimated in August that there were at least 48 million unfinished pre-sold homes in China. Beijing may have nearly doubled its credit support to projects on the “white list,” but the 4 trillion yuan figure falls short of the estimated spending to resolve the unfinished homes issue.

3. Beijing’s attempt to revive the real estate sector is being hampered by broader and more significant economic issues, including:

i) Household incomes are down and people are less inclined to spend on property. Data released by the State Taxation Administration on Oct. 15 showed that 70 percent of individuals with comprehensive income are not required to pay income tax. This means that about 650 million people of China’s 720 million-strong employed population have a monthly income of less than 5,000 yuan.

Meanwhile, local governments facing fiscal shortages are delaying the payment of wages to civil servants. Information circulating in Chinese social media noted that civil servants in Nanjing, the capital of Jiangsu Province, are only guaranteed to receive three months of salary in 2024, with the local authorities striving to issue wages for six or more months.

ii) The rapid deterioration of China’s economy has resulted in more business closures and a sharp rise in unemployment. This in turn has led to an increase in houses being put up for judicial auction (properties that are seized and auctioned off due to loan defaults or to repay debts). The surge in judicial auctions has further driven down property prices.

Falling prices, however, are not attracting people to purchase foreclosed properties. Per data released by China Real Estate Information Corp. (CRIC) on Aug. 12, 2024, the number of residential foreclosure properties listed for auction nationwide in the first half of the year increased by over 12 percent from a year ago to more than 202,000 units. Meanwhile, the transaction rate for foreclosed properties in the first half of 2024 was just 17 percent, down 7 percent from the same period a year ago, while the average discount on sold foreclosed properties reached 33 percent.

iii) Growing geopolitical tensions are impacting China’s economy and reducing external demand. In particular, China’s exports and imports appear to be slowing as the U.S. and its allies gradually decouple (“friendshoring,” supply chain relocation, imposing tariffs, etc.) from China.

iv) Large-scale population decline and an aging population are key factors behind the real estate sector’s loss of momentum and inability to rebound in the long run. Beijing currently lacks effective social security policies to address the crucial population issue.

Beijing’s policies to rescue the real estate sector will be limited if it cannot address deeper and more critical issues. We believe that Beijing will find it exceedingly difficult to turn around the property sector and reverse China’s economic decline so long as it clings to the CCP authoritarian system and the external environment grows more hostile towards the PRC.

2 China’s GDP growth for first nine months of 2024 suggests Beijing’s target is slipping out of reach

On Oct. 18, the National Bureau of Statistics released China’s third quarter GDP and other data.

GDP

- China’s GDP grew by 4.8 percent from a year ago in the first three quarters of the year.

- On a quarterly basis, China’s GDP grew by 5.3 percent in Q1, 4.7 percent in Q2, and 4.6 percent in Q3.

Fixed asset investment (January to September)

- Nationwide fixed asset investment (excluding rural households) increased by 3.4 percent year-on-year (based on a comparable caliber) to reach 3.79 trillion yuan. Private fixed asset investment decreased by 0.2 percent to 1.91 trillion yuan during the same period.

Real estate (January to September)

- Nationwide real estate development investment decreased by 10.1 percent year-on-year (based on a comparable caliber) to reach 7.87 trillion yuan. Residential investment decreased by 10.5 percent to 6 trillion yuan during the same period.

- The sales area of new commercial housing declined by 17.1 percent year-on-year to reach 702.84 million square meters. Residential sales area was down 19.2 percent to 587.88 million square meters during the same period.

- The sales value of new commercial housing decreased by 22.7 percent year-on-year to reach 6.89 trillion yuan. Residential sales value decreased by 24.0 percent to 6.02 trillion yuan during the same period.

Retail sales

- In September 2024, retail sales of consumer goods increased by 3.2 percent year-on-year to reach 4.1 trillion yuan.

- Retail sales excluding automobiles increased by 3.6 percent year-on-year to 3.66 trillion yuan.

- Retail sales of goods by enterprises above designated size increased by 2.8 percent year-on-year to 1.56 trillion yuan.

- From January to September, retail sales of consumer goods increased by 3.3 percent year-on-year to reach 35.36 trillion yuan.

- Retail sales excluding automobiles increased by 3.8 percent year-on-year to 31.8 trillion yuan.

- Retail sales of goods by enterprises above designated size increased by 2.2 percent to 12.6 trillion yuan.

Our take

1. Officials from the National Development and Reform Commission and the Ministry of Finance have recently claimed that the PRC can achieve its 2024 economic growth target. However, Beijing’s own figures show that the growth is slowing every quarter. With various economic indicators trending downward and the recently rolled out economic support measures needing some time before having any real impact, the PRC will likely have to substantially manipulate its data in the following months to hit its “around 5 percent” growth target.

i) China’s “troika” of growth drivers — exports, investment, and consumption — showed weak growth in the first three quarters of the year:

- Exports grew by 4.3 percent year-on-year in the first three quarters per official figures, but just 3.9 percent when compared with the PRC’s own figures in 2023. However, exports fell by 3 percent when compared with figures for the same period from 2022.

- National fixed asset investment grew by just 3.3 percent year-on-year in absolute terms. Private fixed asset investment, which reflects economic activity, declined by 1.2 percent. Compared to the same period in 2019 before the pandemic, the share of private fixed asset investment fell from 57.4 percent to 50.4 percent. Meanwhile, real estate, which previously accounted for nearly a quarter of GDP, saw continued double-digit decline (down 10.1 percent) in development investment in the first three quarters of the year.

- Total retail sales of consumer goods grew by 3.3 percent year-on-year in the first three quarters. The growth in retail sales so far this year is relatively weak compared to growth just before the pandemic (8.2 percent in 2019), during the pandemic years (3.3 percent in 2020, 4.4 percent in 2021, and 2.5 percent in 2022), and just after the end of “zero-COVID” (5.5 percent in 2023).

The underperformance of China’s growth “troika” undercut the official GDP figures reported by the NBS.

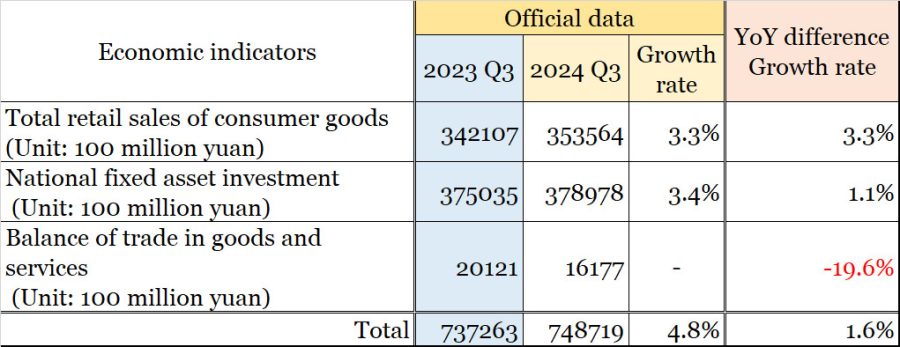

ii) Using a method that the CCP authorities use to calculate real GDP growth, we estimate that China’s GDP growth for the first three quarters of 2024 was actually 1.6 percent, or far below the official figure of 4.8 percent.

Table 1 (Sources: National Bureau of Statistics and State Administration of Foreign Exchange)

In the chart above, we assume that the year-on-year growth rate for balance of trade in goods and services in the first three quarters is the same as in the first half of the year (negative 19.6 percent) since the State Administration of Foreign Exchange has only release balance of trade data for the first eight months of the year.

2. We previously analyzed (see here and here) that Beijing’s recent economic support measures have not addressed key issues behind China’s economic decline (real estate, social welfare, household consumption, etc.) and will take time to be implemented. Therefore, the policies are likely to have a limited impact on China’s economic growth in the fourth quarter.

We believe that the CCP authorities will find it very difficult to hit its “around 5 percent” without creative data manipulation and taking measures to completely change the pessimism about China’s economic prospects both inside and outside the country. Regardless, the NBS will undoubtedly release data next year showing that it had met the growth target.