1 Assessing the fallout of the probe of Zhang Youxia and Liu Zhenli

Zhang Youxia and Liu Zhenli under investigation

Jan. 24

1. Jiang Bin, a spokesman for the PRC Ministry of National Defense, announced at a routine press conference that the CCP Central Committee has decided to open a formal investigation into Zhang Youxia, member of the Politburo and vice chairman of the Central Military Commission, and Liu Zhenli, member of the CMC and Chief of the Joint Staff Department of the CMC.

2. The PLA Daily published a front-page editorial on the probe of Zhang Youxia and Liu Zhenli titled, “Resolutely Win the Tough, Protracted, and Overall Battle Against Corruption in the Military” (堅決打贏軍隊反腐敗鬥爭攻堅戰持久戰總體戰).

The article stated that the investigation into Zhang and Liu once again demonstrates the CCP authorities’ “rock-solid resolve to carry the anti-corruption struggle through to the end,” and their “firm stance of showing no leniency toward anyone, regardless of who they are or how high their position may be, if they engage in corruption.” It described the handling of Zhang and Liu as a “major achievement” in the anti-corruption campaign.

The article noted that Zhang and Liu, who were senior leaders in the Party and the military, had “seriously betrayed the trust and heavy responsibilities entrusted to them by the Central Committee and the Central Military Commission; seriously trampled on and undermined the CMC Chairman Responsibility System; seriously fueled and exacerbated political and corruption problems that weaken the Party’s absolute leadership over the military and endanger the Party’s governing foundations; seriously damaged the image and authority of the CMC leadership; seriously undermined the political and ideological foundation of unity and progress among officers and soldiers across the entire military; caused grave damage to political military-building, the political ecosystem, and the development of combat effectiveness; and produced extremely adverse effects on the Party, the state, and the military.”

The article said that all officers and soldiers must resolutely support the decisions of Party Central, resolutely obey Party Central’s command, the CMC, and General Secretary Xi, and ensure a high degree of centralization, unity, purity, and consolidation within the forces.

The article further explained that the current concentrated crackdown on corruption does not mean that corruption is worsening despite efforts to combat it (越反越腐, “the more it is fought, the more it persists”), but rather that investigations are becoming more thorough (越挖越深, “digging deeper and deeper”). The article also urged the entire military to “resolutely implement the major decisions and deployments of Party Central, the CMC, and General Secretary Xi,” to “unite closely around Party Central with Comrade Xi Jinping at the core,” and to fully implement the “CMC Chairman Responsibility System.”

3. The South China Morning Post cited a source familiar with the matter as saying that the CCP elite had been briefed on the investigation of Zhang Youxia and Liu Zhenli on Jan. 23. The source added that Zhang was “accused of corruption and of failing to rein in his close associates, family members and relatives,” as well as blamed for “not flagging problems to the Party leadership at the first instance.”

A second source said that Zhang was formally detained by the military’s anti-corruption investigators on Jan. 19.

Jan. 25

The Wall Street Journal, citing sources familiar with the matter, claimed that a high-level briefing on the allegations against Zhang Youxia and Liu Zhenli on Jan. 24 claimed that Zhang was being probed for reportedly “forming political cliques,” accepting “huge sums of money in exchange for official promotions” in the big-budget procurement system, and for leaking “core technical data on China’s nuclear weapons” to the United States.

The people familiar with the matter said that some of the evidence against Zhang came from Gu Jun, the former general manager of the state-owned company China National Nuclear Corp., which oversees all aspects of the PRC’s military and civilian nuclear programs. The CCP authorities had announced an investigation into Gu on Jan. 19.

The people also said that the briefing linked Zhang’s case to former defense minister Li Shangfu by alleging that Zhang promoted Li in exchange for large bribes.

Finally, the people noted that Xi has commissioned a task force to carry out a deep-dive probe into Zhang’s tenure as commander of the Shenyang Military Region (2007 to 2012). The task force is reportedly now in Shenyang and has opted to stay in local hotels rather than military bases, “where Zhang would have a network of support.”

Current state of the CMC

The purge of Zhang Youxia and Liu Zhenli means that the only remaining members of the CMC are Xi Jinping (CMC chairman) and Zhang Shengmin (newly promoted CMC vice chairman). The other CMC members have been successively taken out in recent years:

- August 2023: Li Shangfu, a CMC member and defense minister, was investigated.

- November 2024: Miao Hua, a CMC member and director of the CMC Political Work Department, was investigated.

- October 2025: He Weidong, a Politburo member, CMC member, and CMC vice chairman, was expelled from the Party and the military.

When Zhang Youxia’s removal is confirmed, this would be the first time since 1989 that the CCP has purged two sitting Politburo members before the end of their terms. In 1989, the Party removed Zhao Ziyang (then CCP General Secretary and first-ranked CMC vice chairman) and Hu Qili (then Secretary of the Central Secretariat) from the Politburo and its standing committee over their “soft” handling of the Tiananmen Square demonstrations.

Our take

The purge of Zhang Youxia and Liu Zhenli — two active members of the CMC — is the most tumultuous political development to hit the PLA since Xi Jinping came to power. This development appears to be a continuation of the fallout from the PLA Rocket Force scandal in 2023 that led to the downfall of two defense ministers (Li Shangfu and Wei Fenghe) that year, the top military political leader (Miao Hua) in 2024, and nine generals near the end of 2025.

1. The high-level purges almost certainly have a destabilizing effect on the CCP, but are unlikely to shake up CCP elite politics much. The manner in which Zhang Youxia was marginalized demonstrates that Xi Jinping’s power remains, for the time being, beyond challenge. Also, Xi’s grip on the military is strong enough to crush coup attempts and allow him to retain control over the CCP regime; that being said, Beijing’s official characterization of Zhang’s case points to discontent towards Xi in the PLA. Concurrently, Xi’s purge of Zhang mostly debunks persistent rumors that predominantly circulate in overseas Chinese-speaking circles claiming that Xi has “lost power” and has been stripped of control over the military.

One popular belief of the “Xi losing power” camp is that Zhang, with the backing of Party elders, had effectively sidelined (架空) Xi some time in 2025 and is the one who is actually in control of the PLA and the CCP. But if this was indeed the case, then Xi would never be able to purge Zhang as the latter would have almost certainly restricted Xi’s movements and actions (Zhang, after all, supposedly controlled the Party’s all-important “gun”) given the “you live, I die” nature of factional struggles in the CCP elite.

The “Xi losing power” camp’s argument that Zhang Youxia was actually in control becomes even more unpersuasive in considering past precedent. Hu Jintao was genuinely sidelined by Jiang Zemin and the Jiang faction for the bulk of his tenure, and was unable to move against Jiang and his lackeys even after being targeted by multiple assassination attempts despite being CMC chairman. Hu could only go after key Jiang faction lieutenant Bo Xilai in his last year in office due to the seriousness of the Wang Lijun incident and the political earthquake that resulted. The strength of the Jiang faction at the time also meant that Hu could not move against Zhou Yongkang, Bo’s chief accomplice in a coup attempt against Hu, while in office.

2. Officially, the Xi leadership justified its removal of Zhang Youxia and Liu Zhenli on the grounds that they had committed egregious offenses that endangered the CCP regime. The PLA Daily’s Jan. 24 editorial used exceptionally harsh wording and phrases to condemn the two generals, more severe than that used previously against He Weidong and Miao Hua. The official response to Zhang and Liu’s purge was also more rapid than in previous high-level PLA probes, underscoring the gravity of the situation and the urgent need to issue a definitive political line to the entire Party and military.

In the CCP’s political culture, how condemned officials are characterized (定性) is not merely a prelude to a legal trial, but also the core of the final political “verdict.” It determines the historical standing of the purged official, the fate of their associates, and the specific “lessons” the entire Party and military are expected to internalize. Categories of characterization include:

- Disciplinary violations (違紀): Breaches of Party rules. Considered an internal organizational matter.

- Legal violations (違法): Breaches of state law. Typically refers to bribery or corruption.

- Political problems (政治問題): Fundamental deviations involving political line, policy, or loyalty.

- Usurping Party power/splitting the Party (篡黨奪權/分裂黨): The highest level of political accusation, implying a direct challenge to the CCP’s supreme authority.

When the PRC defense ministry announced the probe of He Weidong, Miao Hua, and seven other generals in October 2025, it used the following phrases in characterizing them:

- “Serious violations of Party discipline.”

- “Suspected of serious duty-related crimes.”

- “Extremely large amounts involved.”

- “Extremely serious in nature.”

- “Extremely adverse impact.”

While severe, the accusations against the nine generals remained within the realm of duty-related crimes. By contrast, the accusations against Zhang and Liu venture into the political realm:

- “Seriously trampling on and undermining the CMC Chairman Responsibility System”

- This entails that Zhang and Liu had potentially overrode Xi’s command authority on certain matters, sanctioned unauthorized troop movements, concealed major military intelligence, or refused to execute Xi’s orders. Since Zhang oversaw military operations and Liu controlled the Joint Staff Department (the “nerve center” of the PLA), they are de facto being “mutiny” or “insurrection.”

- “Seriously fostering and exacerbating political and corruption problems that undermine the Party’s absolute leadership over the military and endanger the Party’s governing foundations.”

- The accusation of “endangering the Party’s governing foundations” suggests that what Zhang and Liu did represented an existential, deep-seated threat to the CCP. This implies that Zhang and Liu’s “clique” sought more than financial gain, and had potentially formed an “independent kingdom” (wide-spanning interest network) capable of rivaling Party Central. It is not implausible that the duo were indeed behind an interest group that could endanger the regime as Zhang is a Party princeling with rare combat experience (giving him valuable political credentials in the CCP) and Liu controlled the PLA’s operational command system.

- “Seriously damaging the image and authority of the CMC leadership.”

- The actions of Zhang, Liu, and other generals in the 20th CMC — which Xi handpicked — have led to the dismantling of nearly the entire CMC membership. This represents a severe blow to Xi’s “quan wei” (authority and prestige).

- “Seriously undermining the political and ideological foundation of unity and progress among officers and soldiers across the entire military.”

- This indicates that the downfall of Zhang and Liu is psychologically damaging to the PLA. Before their investigation, members of the 20th CMC were responsible for the military’s political indoctrination. Now those who were considered to be loyal to Xi are accused of betraying him. In particular, Zhang’s “betrayal” — as a family friend of Xi and a representative of the “second generation reds” — has shattered the myth that the princelings are loyal to Xi and fundamentally shakes the military’s belief in the political ethics of the top leadership.

- “Causing extremely serious damage to political military-building, the political ecosystem, and the development of combat effectiveness.”

- The nine generals were accused of damaging the “political ecosystem,” whereas Zhang and Liu are accused of much more. This characterization essentially designates Zhang and Liu as “political enemies” (政治敵人) of the Party, while He, Miao, and others are only at the level of “two-faced individuals” (兩面人).

- “Causing extremely adverse effects on the Party, the state, and the military.”

- The collective and widespread corruption of the PRC’s highest-ranking generals expose the failures of the Xi leadership’s efforts at political indoctrination and the anti-corruption campaign.

3. We are skeptical about some of the information about Zhang Youxia’s case that has been reported in English language media.

In the case of the South China Morning Post, the newspaper is owned by the Alibaba Group and leans pro-Beijing. It cannot be ruled out that the details about Zhang’s alleged offenses that SCMP reported are part of the CCP’s attempt at damage control by “leaking” a sanitized version of what the general is being investigated for.

Meanwhile, The Wall Street Journal’s information about Zhang Youxia supposedly leaking nuclear secrets to the U.S. is reminiscent of an earlier allegation involving another purged official. In December 2026, Politico claimed that Qin Gang and “relatives of top rocket force officers had helped pass Chinese nuclear secrets to Western intelligence agencies.” However, we noted that the allegation was unlikely as Qin “would not be able to obtain them in his capacity as foreign minister and is very unlikely to have ample opportunities in the foreign service to cross paths with senior PLA officials who would be privy to such classified information.” We also expressed skepticism that Qin had “died, either from suicide or torture” as Politico claimed; our assessment was subsequently affirmed when Qin made a public appearance in October 2025.

The allegation that Zhang divulged nuclear secrets is slightly more believable because he would be able to access them as CMC vice chair. But given that Zhang holds such a senior post and is virtually unable to leave China, leaking classified information would carry risks vastly disproportionate to any potential gains for him, leaving him with virtually no incentives to take such action.

4. A senior cadre of Zhang Youxia’s standing — notably, a member of the “red aristocracy” with family connections to the paramount leader — would typically be afforded a “soft landing” even if they are guilty of serious corruption or poor performance. This is particularly so in considering that leaders who purge those whom they themselves promoted are engaging in self-indictment by the act. A combination of factors likely contributed to Xi Jinping’s decision to remove Zhang.

i) The removal of Zhang Youxia is the logical outcome of the Xi leadership’s investigation into the PLARF scandal in 2023 and efforts at “rectifying” the situation. The PLARF scandal led to probes of the corruption-prone equipment development system, where Zhang headed from 2012 to 2017 (PLA General Armaments Department, 2012—2015; CMC Equipment Development Department, 2015—2017). It is likely that anti-corruption investigators either discovered or were fed information concerning Zhang’s corruption during that period.

Xi’s willingness to take out Zhang over allegations of his corruption suggests that he must have been very frustrated by persistent and severe setbacks to his vision of transforming the PLA into a modern fighting force capable of power projection to match the PRC’s ambitions and taking Taiwan should the need arise.

ii) The nonstop revelations since 2023 that those whom Xi considers to be loyalists are in fact very corrupt and/or have undermined his agenda with their actions could have greatly heightened Xi’s paranoia and induced him to order purges that he previously could have second thoughts about undertaking. In turn, Xi’s willingness to purge his allies could have caused some of them to become more guarded and engage in suspicious activities (banding together, coordinating testimonies, or seeking protection from other political patrons) that would further fuel Xi’s paranoia and distrust. This creates a vicious cycle that would ultimately lead Xi to take out Zhang Youxia and potentially result in Stalin-style purges (if they are not already happening) in the military and the officialdom.

iii) Xi could be buying his own propaganda about “self-revolution” and “turning the knife inward.” By not declaring a conclusion to his anti-corruption campaign, Xi has to endlessly hold up “tigers and flies” to demonstrate the existence of corruption and vindicate his decision to be “always on the road” in struggling against it. This in turn incentivizes Xi’s investigators to go hunting for corruption everywhere, including on the persons of Xi’s own allies and loyalists. The discovery of yet more corruption will further convince Xi of the “rightness” of his ways and deepen his distrust of those around him, perpetuating the “self-revolution” cycle.

iv) Xi could have been manipulated by his political enemies and other discontents into purging Zhang Youxia and other allies. The CCP’s intelligence apparatus in particular was swayed by Zeng Qinghong and the Jiang faction, and could have had a hand in feeding “damning” information about Zhang and others to anti-corruption investigators or directly to Xi himself. External “anti-Xi” elements, including those who advocate a strategy of leadership change in China and foreign intelligence agencies, could also have had a hand in shaping the international information environment to influence the CCP intelligence apparatus’s assessments. For instance, the external information environment has continually cast doubt on Xi’s control over the PLA and the CCP (over the past two years) while lionizing “opposition” figures like Zhang Youxia (at least over the past year). There also appears to be a tremendous amount of information circulating about supposed fractures in the CCP elite during a period where actual factional struggle activity is at a low point following Xi’s power consolidation at the 20th Party Congress.

A highly paranoid Xi would be especially susceptible to “intelligence” that his allies and loyalists are betraying or about to betray him, and be more inclined to take action that makes himself more vulnerable to his real enemies. We previously wrote that “Xi Jinping’s remaining factional rivals and the ‘anti-Xi coalition,’ including elements opposed to Xi in the military or the CCP intelligence apparatus’s ‘hidden front’ (see here and here), to exploit the Xi leadership’s prioritization of national security matters to ‘manipulate’ the PRC leader into taking out his own allies and ultimately undermining his own interests.”

v) It cannot be entirely ruled out that Zhang Youxia had indeed attempted to move against Xi Jinping, but was unsuccessful. This would leave Xi with no choice but to purge Zhang now instead of letting him retire before the 21st Party Congress.

5. The downfall of Zhang Youxia and Liu Zhenli will produce a chilling effect across the PLA, the CCP bureaucracy, and among the “red aristocracy.”

i) The CMC has been effectively reduced to the “one-man rule” of Xi Jinping. Newly promoted CMC vice chairman Zhang Shengmin, who was previously the PLA’s discipline inspection chief, could be made to prioritize the overseeing of anti-corruption work in the military while broadly covering the roles (military affairs and political work) of the purged CMC vice chairmen. In a sense, the CMC has been transformed into an “expanded discipline inspection committee” with professional military decision-making potentially being supplanted entirely by political vetting.

ii) As chief of the Joint Staff Department, Liu Zhenli was responsible for coordinating joint operations across all theater commands and service branches. His investigation means that the top-level design of the entire combat command system, emergency contingency plans, communication codes, and even nuclear button protocols may face scrutiny and reset. While second-line officers have undoubtedly been tapped to take over Liu’s responsibilities, the PLA has entered a temporary state of “brain death” until the Xi leadership finds a permanent replacement and concludes probes associated with Liu in the Joint Staff Department.

iii) A power vacuum is likely to emerge within the PLA’s command hierarchy. The unofficial scale of Xi’s purge of the senior ranks of the military could be quite significant, particularly among the lower general ranks. Newly promoted generals (such as Yang Zhibin and Han Shengyan) likely have insufficient “quan wei” or influence to immediately command respect down the ranks. Meanwhile, officers at all levels could start to engage in mutual denunciations for self-protection, driving down unit cohesion and morale.

iv) Mid-to-senior level officers could become even more passive and bureaucratic as they search for political survival in an environment where they feel that even the slightest mistakes get severely punished. Officers could also attempt to pass the buck on making the final call on issues such as equipment procurement and exercise planning, thereby lowering the PLA’s administrative and training efficiency. Such behavior in the PLA will eventually seep over into the civilian side, impacting the CCP’s governing efficacy on the whole.

v) The rise of political work and disciplinary cadres like Zhang Shengmin could create a situation where those who carry out purges enjoy easier paths to promotion that those who undertake the comparatively harder task of military modernization. This could lead to the marginalization of professional officers who excel in military affairs, while cadres skilled in political opportunism occupy high-level positions. Over time, this will seriously degrade the PLA’s professional quality.

vi) Xi Jinping’s purge of Party princeling and family friend Zhang Youxia signals to the “red aristocracy” that none of them are safe anymore. This could silence some of the criticisms of Xi and his policies that undoubtedly are voiced as princeling gatherings. However, the bulk of “anti-Xi” elements will unlikely be intimidated into ceasing their resistance towards Xi, and could adopt greater caution to circumvent surveillance.

6. The PLA will likely be temporarily “blunted” as a fighting force while Xi Jinping is subjecting it to Stalin-style purges and brainwashing. Notably, the removal of Liu Zhenli, the replacement of several theater commanders, and ongoing efforts to rectify corruption in the equipment development and political departments will likely prove disruptive to military operations and major plans. The PLA will need some time to get itself back up to speed to be able to undertake complex military operations such as an invasion of Taiwan.

While the PLA’s leadership and organization are currently in disarray, it should not be discounted as a threat. Xi’s goal with the high-level purges and intensification of political indoctrination is to strengthen the PLA. Also, the CCP’s effort to modernize and expand the military continues apace in various areas (such as shipbuilding, fighter building, and missile development) even as the top level of the PLA is being subjected to rectification. Should Xi find even a modicum of success in rooting out systemic issues contributing to corruption, the PLA could emerge from the current debacle as a more professional, proficient, and reliable fighting force in the future.

Amid the current chaos, the PLA still has the ability to play a role in the CCP’s external behavior. The PLA will likely continue mostly unabated with its drills, harassment, intimidation, and gray zone operations in the South China Sea, East China Sea, and the Taiwan Straits. And while an invasion is unlikely, the PLA still possesses the operational conditions to implement a “quarantine” or “blockade” of Taiwan. An “inhibited” PLA is also dangerous in the currently very low-probability scenario where Xi Jinping becomes highly irrational and decides to invade Taiwan or launch/join a war elsewhere to create external distractions to relieve an intense build-up of internal pressures as various crises facing his leadership come to a head.

2 Analyzing the 2026 liquidity upheaval in China’s banking sector

50 trillion yuan of time deposits maturing in 2026

According to forecasts by multiple Chinese financial institutions and analyses of market data, around 50 trillion yuan ($7 trillion) in time deposits and large-denomination certificates of deposit are expected to mature in 2026. This massive pool of funds was accumulated during the peak of “precautionary saving” from 2020 to 2023 when households locked in high-yield, long-term deposit products to hedge against economic uncertainty.

Based on 2025 interim financial data from the six major state-owned banks, Guosen Securities estimates that time deposits maturing within the next year account for 38.0 percent of total deposits and 62.8 percent of all time deposits at these banks, with maturities concentrated between late 2025 and early 2026. On this basis, the scale of time deposits maturing in 2026 is estimated at around 57 trillion yuan, with the bulk maturing in early 2026.

CITIC Securities estimates that the volume of two-year and longer-term time deposits maturing in 2026 across the entire economy could reach 45 trillion yuan. More than 35 trillion yuan consists of three-year deposits that were heavily issued in 2023.

China International Capital Corporation (CICC), drawing on deposit repricing structures at 42 A-share listed banks, estimates that 32 trillion yuan in long-term household time deposits (two years or longer) will mature in 2026 (4 trillion yuan more year-on-year). Of the total, 61 percent of these deposits are likely to mature in the first quarter.

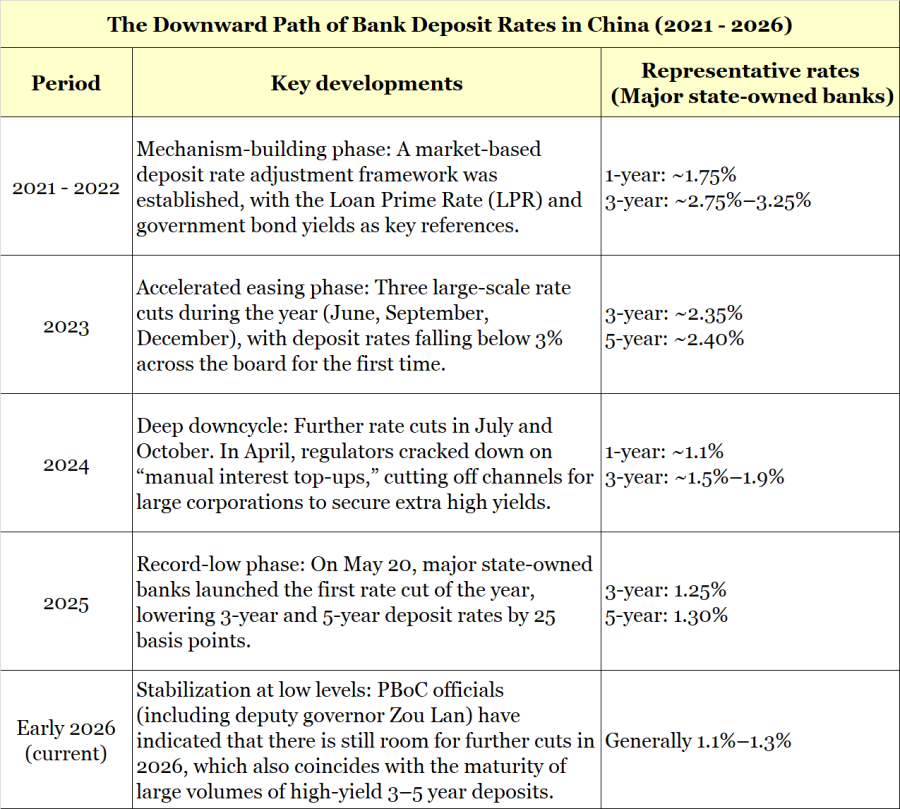

Chinese bank rate cuts between 2021 to 2026

Over the past five years, bank deposit rates in China have fallen from “above 3 percent” to what is now widely described as the “1 percent era.”

Specific ways banks restrict fixed deposits with maturities over three years

PRC regulators have effectively rendered long-term deposits (especially 5-year tenors) nominal and obsolete through a combination of market self-discipline and business guidance.

Supply cuts and shorter tenors for large-denomination certificates of deposit (CDs)

Since 2024, major state-owned banks — including Industrial and Commercial Bank of China, Agricultural Bank of China, Bank of China, China Construction Bank, and Bank of Communications — have largely stopped offering 5-year large-denomination CDs. Quotas for 3-year CDs are often snapped up instantly or made available only to select new customers. Currently, most large-denomination CDs with a minimum investment of 200,000 yuan are limited to maturities of two years or less.

Rate ‘inversion’ and ‘flattening’

To reduce long-term funding costs, banks deliberately set 5-year deposit rates at the same level as 3-year rates (currently both around 1.25 percent to 1.3 percent). Some small and medium-sized banks have even seen “inverted” yield curves, where 5-year rates are lower than 3-year rates, discouraging households from locking in long-term deposits.

Crackdown on ‘manual interest top-ups’

In April 2024, the market-based interest rate pricing self-discipline mechanism explicitly prohibited banks from using offline compensation or “manual interest top-ups” to circumvent deposit rate ceilings. As a result, many long-term negotiated deposits that were officially quoted at 2.5 percent but privately topped up to around 3.5 percent were forcibly unwound.

Cancellation of certain long-term products

From the second half of 2025 onward, many regional and small banks announced the formal cancellation of 5-year fixed-term deposit products, citing “asset–liability matching needs.”

Our take

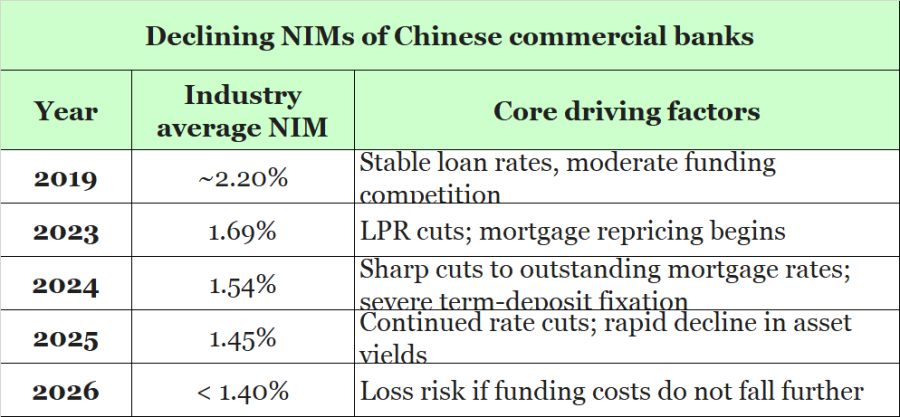

1. China’s financial system is set to undergo an unprecedented liquidity reshuffle in 2026, with an estimated 50 trillion yuan in high-interest assets maturing. This shift is driven by the Chinese banking industry’s strategic cancellation of long-term CD products and aggressive cuts to deposit rates, as banks grapple with the dire challenge of Net Interest Margins (NIM) falling below the 1.5 percent warning line.

The series of monetary and financial policies implemented by Beijing — suppressing deposit rates and eliminating high-yield deposit-gathering tools — is not only aimed at easing NIM pressure and mitigating local government debt risks. On a deeper level, it reflects a classic strategy of financial repression. The core logic of this strategy is to artificially depress the nominal returns on risk-free assets, theoretically creating an environment that “penalizes” cash holders. This is intended to force massive household and corporate savings to flow into real-economy investment or consumption, thereby breaking the deadlock of economic stagnation.

However, against the backdrop of China’s deepening structural deflation, this strategy faces a serious risk of failure and may even generate a liquidity-trap effect opposite to policymakers’ intentions. China’s household sector is more likely to exhibit a strong income effect, rather than the substitution effect policymakers expect. Confronted with declining asset yields and uncertainty over future income, households have not increased consumption; instead, they have raised their savings rates to secure future financial buffers. This has led to a historically rare widening “scissors gap” between M2 and M1 growth.

2. The 50 trillion yuan in deposits maturing in 2026 represents a carefully orchestrated macro-financial strategy by Beijing to rescue China’s banking sector. It aims to address systemic banking risks through financial repression and to forcibly reshape the asset-allocation structure of households.

i) The 50 trillion yuan in time deposits that are expected to mature over the year (per the combined estimates of CICC and Guosen Securities) is not only a record high in absolute terms but also staggering in its scale — representing nearly one-third of total household savings facing repricing.

This capital did not appear out of thin air. It is the product of a specific historical window from 2020 to 2022. During that period, the Chinese economy was hit by repeated shocks caused by “zero-COVID” policies, a deep adjustment in the property market (symbolized by China Evergrande’s default), and the painful transition toward net-asset-value–based wealth-management products that broke implicit guarantees. During this period, Chinese households underwent a sharp shift toward risk aversion:

- The disenchantment with real estate: The two-decade expectation of a housing bull market collapsed, leading households to park what would have been home down payments into bank deposits.

- The shock from net-asset value-based wealth management: After new asset-management regulations, wealth management products were no longer principal-protected and became more volatile, driving conservative capital back into on-balance-sheet deposits.

- Locking in high yields: From 2020 to 2022, Chinese commercial banks, competing aggressively for liquidity, issued large volumes of three- and five-year certificates of deposit with interest rates of 3.5 percent or even above 4.0 percent.

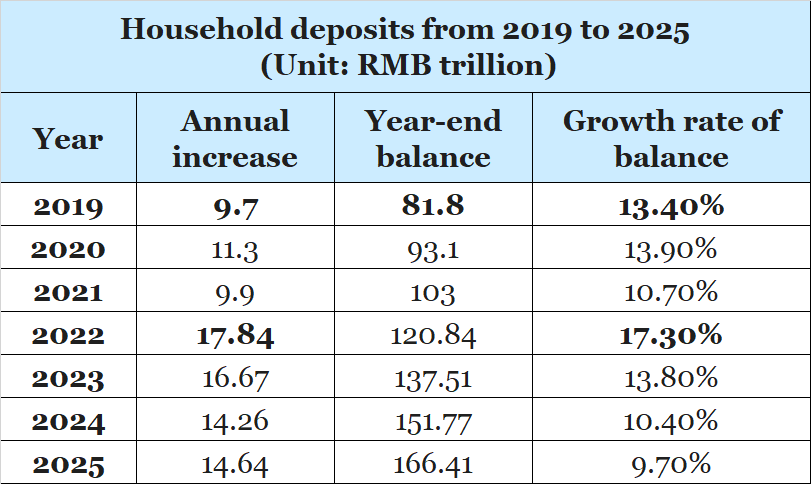

The PBoC’s financial statistics reports over the years show that household deposits in China grew significantly between 2019 and 2025, with a record annual increase in 2022.

ii) To support the real economy, Beijing has continuously guided lending rates (LPR) downward in recent years. Banks have also been required to purchase large volumes of debt-swap bonds at extremely low yields (around 2 percent) to defuse local government debt risks. The cliff-like drop in asset-side yields has forced banks to aggressively compress funding-side costs. Yet cutting rates has pushed banks’ net interest margins into dangerous territory.

Regulators have traditionally viewed a NIM above 1.8 percent as necessary. By late 2024 and early 2025, however, the industry average had fallen to around 1.5 percent, with some major state-owned banks as low as 1.42 percent. This threatens banks’ internal capital generation. Without sufficient retained earnings, banks cannot replenish core Tier-1 capital, constraining future lending and impairing their ability to absorb non-performing loans arising from the property crisis.

The rapid deterioration in asset quality has triggered large-scale consolidation among small and medium-sized banks, temporarily masking systemic risks. According to Enterprise Early Warning risk tracking platform and financial media statistics, 2025 marked the highest number of bank exits in China’s history: by Dec. 26, 394 banking institutions had exited the market through mergers or dissolutions, or double the number in 2024. Over 2024 and 2025, nearly 550 banks disappeared via restructuring, exceeding the total of the previous seven years combined.

By canceling CDs, banning “manual interest top-ups,” and repeatedly cutting posted deposit rates, the CCP authorities aim to forcibly reduce funding costs — paying depositors less interest — to preserve bank profitability. While this appears to be about “saving banks,” more fundamentally the move is about preserving banks’ role as the core channel for debt swaps, ensuring their capacity to absorb low-yield local government bonds and thus maintain the appearance of macro leverage stability.

iii) Beyond rescuing banks, Beijing’s financial repression strategy is also intended to stimulate economic circulation by artificially suppressing risk-free rates. This pushes real interest rates (nominal minus inflation) toward zero or even negative, thereby “penalizing” cash and deposit holdings.

Beijing’s logic appears to be as follows:

- Forcing deposits into the real economy: By reducing deposit yields to meager levels (e.g., 1.5 percent), the CCP authorities hope households will stop hoarding cash and instead consume or invest in real businesses, breaking the deflationary spiral.

- Guiding funds into equities (a “slow bull”): By eliminating high-yield deposits, policymakers seek to push moderately risk-tolerant capital into equities — especially high-dividend, “China-specific valuation” central SOE stocks — supporting SOE financing and repairing household balance sheets via rising stock prices.

- Supporting “new quality productive forces”: The authorities hope to redirect idle funds trapped in the banking system into bonds and equity markets toward strategic sectors such as semiconductors, AI, and green energy.

These mechanisms have worked in past cycles. After the 2008 financial crisis, major central banks used quantitative easing and zero-rate policies to lift asset prices and stimulate demand. Beijing clearly hopes to replicate this path by making deposits “unprofitable” so as to push as much as 160 trillion yuan in household savings into equities or real estate, and leverage wealth effects to revive consumption and halt economic decline.

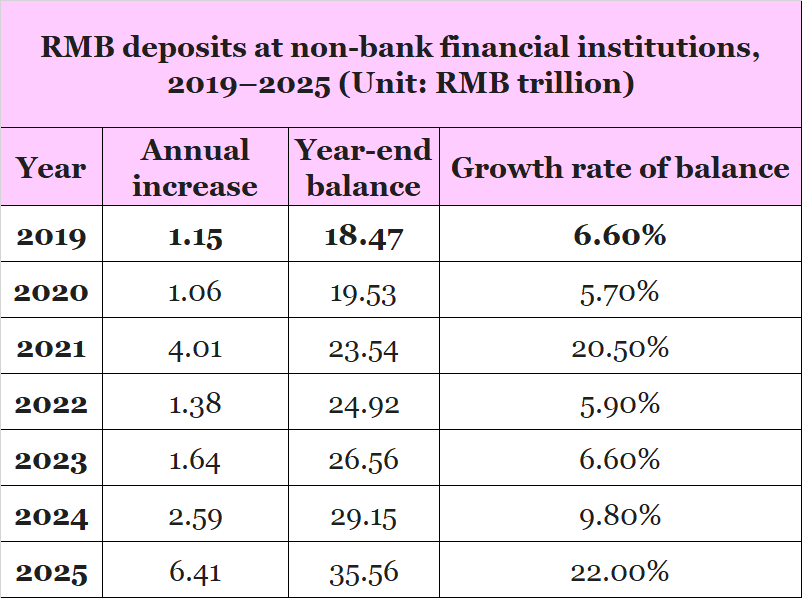

Beijing’s financial repression strategy showed signs of traction in 2025. PBoC data show that non-bank financial institution deposits rose by 6.41 trillion yuan in 2025 — 3.82 trillion yuan more than in 2024 (a 147 percent increase in incremental terms), surpassing previous records in 2015 (4.08 trillion) and 2021 (4.01 trillion). This indicates substantial funds had flowed out of traditional bank savings into securities, funds, and wealth management products.

Beijing’s macro strategy, however, rests on the crucial assumption that inflation expectations exist, or at least that price levels remain stable. If this condition fails, the entire transmission chain of financial repression risks breaking down.

3. Against the backdrop of China’s economy being deeply mired in structural deflation, financial repression faces a severe risk of failure. It may even generate a “liquidity trap” effect that is the exact opposite of policymakers’ intentions.

i) China is currently facing entrenched deflationary pressures that are structural rather than cyclical or short-term.

Persistent weakness in the producer price index

China’s PPI has remained in negative territory for an extended period per official data. In December 2025, PPI fell 1.9 percent year-on-year, following several months of negative readings (for example, negative 2.2 percent in November). Sustained negative PPI growth reflects severe overcapacity in the industrial sector. Declining upstream prices continuously transmit downstream, compressing profit margins across the entire value chain and forcing firms to cut costs, freeze hiring, or even lay off workers. This in turn suppresses expectations for household income growth.

Warning signs from the GDP deflator

Compared with CPI — which is heavily influenced by food prices (especially the pork cycle) — the GDP deflator better captures the overall price level of the economy. Data indicates that China’s GDP deflator has been negative for three consecutive years, the longest period of economy-wide price declines since the late 1970s. This means nominal GDP growth is lagging real GDP growth. Consequently, businesses and individuals experience a subjective sense that money is “harder to earn,” reflecting a decline in micro-level economic vitality.

Structural weakness in the consumer price index

Although CPI rose 0.8 percent year-on-year in December 2025, core inflation (excluding food and energy) stood at only 1.2 percent and hovered near zero in multiple months. In such a low-inflation or even deflationary environment, “cash is king” is no longer a slogan but a rational financial choice.

ii) In a deflationary environment, attempts to “penalize” cash by lowering nominal interest rates are offset by falling prices, which could in turn lead to a reverse tightening effect.

For a manufacturing firm whose factory-gate prices decline by 2 percent annually (PPI = negative 2 percent), even if bank lending rates fall to 3 percent, the real interest rate it faces is as high as 5 percent. This severely suppresses investment incentives for companies. Firms prefer to repay debt (deleverage) rather than take on new loans for expansion, directly leading to a contraction in credit demand.

For ordinary consumers, even though bank deposit rates are only around 1 percent, if the prices of assets they plan to purchase (such as housing, cars, or home appliances) are falling at 5 percent or even 10 percent per year, the “implicit return” on holding cash is effectively 6 percent or even 11 percent.

Thus, in a deflationary context, efforts to penalize cash by depressing nominal interest rates not only fail but actually cause real interest rates to rise passively, as the drop in prices exceeds the rate cuts. Cash, rather than being penalized, becomes the highest-quality asset class due to its “negative correlation” with falling asset prices.

iii) China’s monetary policy transmission mechanism is clearly failing, most visibly reflected in the divergence between M1 and M2 growth, or the so-called “scissors gap.”

M2 (broad money): Includes household savings deposits and corporate time deposits, representing the total money supply.

M1 (narrow money): Mainly includes cash in circulation and corporate demand deposits, representing actively transacting funds.

During the 2024 to 2025 period, M2 maintained relatively strong growth (around 8.8 percent), indicating that the central bank continued injecting base money to keep liquidity ample. However, M1 growth kept declining and even turned negative, pushing the M1–M2 gap to a historical high.

An expanding scissors gap implies:

- Idle circulation of funds: Liquidity released by the central bank is not converted into corporate demand deposits for production and investment, but instead sinks into time deposits within the banking system, or so-called “deposit termization.”

- Lack of confidence: Firms shifting funds from demand to time deposits signal pessimism about the future business environment, preferring to lock in meager interest income rather than retain liquidity for expansion.

- Liquidity trap: This is precisely the “liquidity trap” described by John Maynard Keynes — no matter how much money the central bank supplies, it is hoarded by the public due to liquidity preference or risk aversion, causing the velocity of money to collapse and monetary policy stimulus to the real economy to approach zero.

iv) Beijing’s financial repression strategy is likely to generate a strong “income effect” among households, rather than the “substitution effect” policymakers hope for.

- Substitution effect: Lower interest rates lead to lower opportunity cost of current consumption, which in turns leads to less saving and more consumption (the desired outcome).

- Income effect: Lower interest rates lead to reduced interest income on existing savings, which in turn leads to households having higher savings and reduced consumption in order to maintain future consumption levels or asset accumulation goals.

Chinese households generally exhibit strong “target saving” behavior, saving primarily to meet rigid future expenditures such as education, medical costs, and insufficient pensions. Paradoxically, interest rate cuts have led to a passive compression of current consumption. The lower the interest rate, the higher the “precautionary savings” undertaken to maintain a sense of security. The continuous increase in Chinese household deposits throughout 2025 demonstrates that despite interest rates hitting record lows, the total household savings rate remains high at around 36 percent of disposable income, with no significant decline. By stripping residents of their property-based income (interest), financial repression policies are effectively forcing the population to “tighten their belts” to compensate for the loss. This runs directly counter to Beijing’s strategic goal of expanding domestic demand.

v) Severe wealth polarization in China further undermines financial repression, intensifying the income effect and suppressing consumption.

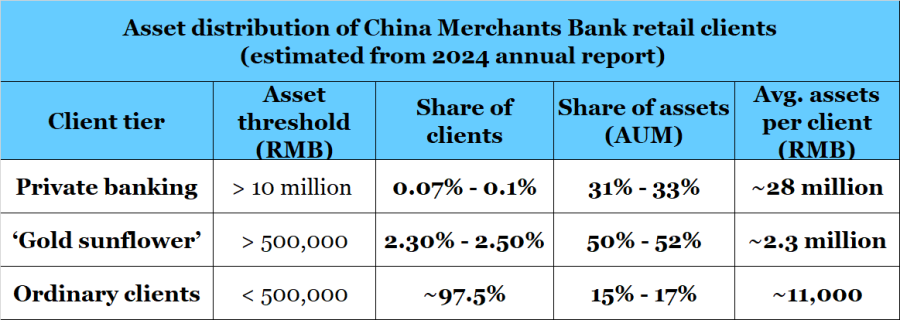

According to China Merchants Bank’s 2023 and 2024 financial reports, wealth concentration in China far exceeds the traditional “20/80 rule” (where 20 percent of the population controls 80 percent of the wealth), and has likely evolved into an extreme “2 percent/80 percent” or even “1 percent/90 percent” structure.

China Merchants Bank classifies retail clients into three tiers: ordinary clients; “gold sunflower” clients (average daily assets > 500,000 yuan); and private banking clients (average daily assets > 10 million yuan). The latest data reveal a striking pyramid:

The above data shows:

- Extreme top concentration: Less than 0.1 percent of private banking clients control roughly one-third of total assets. Their average per-capita assets are more than 2,500 times those of ordinary customers.

- Dominance of the affluent: “Gold Sunflower” and higher tier clients (about 2.5 percent of clients) together control over 82 percent of total assets, leaving the remaining 97.5 percent of ordinary clients with less than 18 percent of the asset “cake.”

- Ordinary households’ asset position: The average assets per ordinary customer are only just over 10,000 yuan. Considering this includes all financial assets such as savings and wealth management products, it indicates that the vast majority of ordinary families have extremely weak financial resilience against economic risks.

Based on this structure, it can be inferred that of the 50 trillion yuan in deposits maturing in 2026, more than 40 trillion yuan is effectively held by less than 3 percent of the population. This explains why simple interest rate cuts fail to stimulate consumption. For the wealthy with tens of millions in assets, a drop in deposit rates from 3 percent to 1.5 percent merely pushes funds into trusts, private equity, overseas assets, or high-end insurance; it does not prompt them to buy more cars or eat more meals. This is the micro-level foundation of China’s current “liquidity trap”: the transmission mechanism of monetary policy breaks down in the face of extreme income and wealth inequality.