1 NBS fudges figures to ‘save’ the economy

Oct. 18

The PRC National Bureau of Statistics released China’s economic data for the first three quarters of 2023.

Some noteworthy data include:

- China’s GDP grew by 5.2 percent year-on-year to 91.3027 billion yuan in the first three quarters of the year. By quarter, China’s GDP increased by 4.5 percent in the first quarter, 6.3 percent in the second quarter, and 4.9 percent in the third quarter (compared with 4.4 percent growth in the third quarter per a Reuters poll).

- Retail sales grew 6.8 percent year-on-year to 34.2107 trillion yuan in the first three quarters of 2023.

- National fixed-asset investment (excluding rural households) grew 3.1 percent year-on-year to 37.5035 trillion yuan in the first three quarters of 2023, or up 6 percent after deducting price factors.

- Investment in infrastructure was up 6.2 percent year-on-year, investment in manufacturing was up 6.2 percent, and investment in real estate development was down 9.1 percent.

- Sales area of commercial housing was down 7.5 percent year-on-year to 848.06 million square meters, while total sales were down 4.6 percent to 8.907 trillion yuan.

- The consumer price index (CPI) grew by 0.4 percent year-on-year in the first three quarters of 2023. In September, the CPI remained at the same level year-on-year and increased by 0.2 percent month-on-month.

- Producer prices for industrial products fell by 3.1 percent year-on-year in the first three quarters of 2023. Prices in September were down 2.5 percent year-on-year.

- Purchasing prices for industrial producers were down 3.6 percent year-on-year in the first three quarters of 2023.

The NBS said that China is on track to hit the PRC’s annual GDP growth target of 5 percent if the GDP grows by more than 4.4 percent in the fourth quarter of 2023.

The NBS also said, “The national economy continued to recover and improve in the first three quarters [of 2023], with high-quality development advancing solidly. This lays a solid foundation for realizing [the PRC’s] annual development goals. However, it should also be noted that the external environment has become more complex and severe, domestic demand is still insufficient, and the foundation for economic recovery still needs to be consolidated.”

Western reaction

Western media were optimistic about China’s economic data for the first three quarters of the year, with news outlets describing the GDP report as “strong,” claiming that China’s economy had “turned a corner,” or describing China’s economic recovery as “gaining traction.”

On Oct. 18, JP Morgan, Nomura, and Citigroup raised their forecasts for China’s economic growth for the year to 5.2 percent, 5.1 percent, and 5.3 percent, respectively.

No restrictions on foreign investments to manufacturing

Oct. 8

At the opening of the Belt and Road Forum for International Cooperation in Beijing, Xi Jinping said that the PRC will lift all restrictions on the flow of foreign investments to the production sector.

PRC propaganda

Oct. 19

State mouthpiece Xinhua published a commentary article titled, “[The Economy] Continues to Improve, Putting to Rest the ‘China Economic Recession Theory’” (持續向好,「中國經濟衰退論」可休矣!).

The commentary argued that JP Morgan and Nomura raising their China GDP forecast for the year after the release of the economic data “fully shows” that the international community “deeply feels” the “continuous and overall recovery” of China’s economy.

The commentary also cited bullish analysis of China’s economy by the international press in slamming the United States for stepping up efforts to contain China over the past several months, including setting up trade barriers through executive orders, “building walls to investment” by exaggerating market risks, and keeping companies away from China “by the hand of power.” The commentary added, “It has been proven that the confidence of international companies in the Chinese market is far from being changed by a single decree of the U.S. government.”

In its conclusion, the commentary noted that “unstable factors facing the global economy are increasing,” but China is “contributing valuable certainty.” While the Chinese economy is “currently facing some challenges,” its “long-term fundamentals will not change.”

Our take

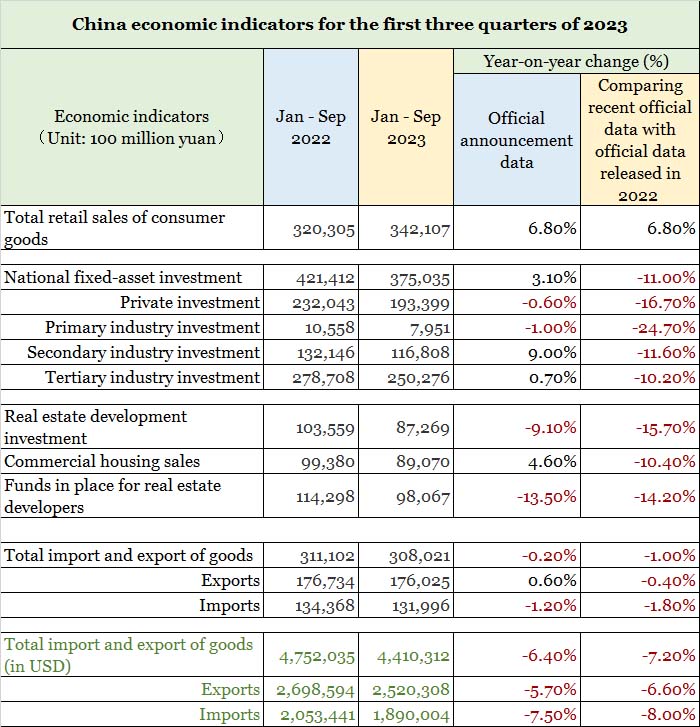

1. Taken at face value, the PRC’s official data for the first three quarters of the year and Q3 GDP growth suggest that China’s economic deterioration is “stabilizing” and even “turning the corner.” However, a simple comparison of the recent official data with the PRC’s own data from last year shows that the Chinese economy more likely than not saw steep decline, not recovery, over the past three quarters.

Source: PRC National Bureau of Statistics and the General Administration of Customs

Data from the table above shows that China’s “troika” of growth drivers—exports, investment, and consumption—appear to have stalled.

The NBS claimed that national fixed-asset investment in China went up by 3.1 percent from a year ago in the first three quarters of 2023. However, the same data when compared to the CCP’s own figures from last year shows a drop in fixed-asset investment by 11 percent. All key investment indicators also saw double-digit percentage declines.

As for consumption, the NBS gave the figure of 6.8 percent growth for the first three quarters of the year, or the same growth rate as in 2022. However, the 6.8 percent figure is hardly believable considering that China’s CPI barely grew over nine months; the CPI rose at a rate lower than 0.3 percent from April to September 2023, and even fell by 0.3 percent in July. Another indicator that consumption was lackluster is China’s M2 money supply growing by just 27 trillion yuan at the end of September 2023 as compared to a year ago; after taking depreciation into account, the 10.3 percent growth in the M2 hints at declining rather than increasing consumption.

China’s exports, which are arguably the central pillar of the growth “troika,” have been particularly dismal. Over the first three quarters of 2023, China’s exports grew just 0.6 percent by the official data, but fell 0.4 percent when compared to official data from the previous year and dropped by 6.6 percent in dollar terms. Exports also fell by 6.2 percent in September for the fifth straight month of declines, and foreshadow further drops going forward.

2. Businesses, investors, and governments should always be very skeptical of the PRC’s official data given the CCP’s habit of falsifying economic numbers. The CCP authorities have admitted that local governments (Tianjin, Inner Mongolia, Liaoning, etc.) have faked economic data (fiscal revenues, GDP, etc.) on a number of occasions (e.g., see here, here, and here), and Beijing held a meeting in May 2022 on the issue of “runaway statistical falsification.”

We have also repeatedly called out the CCP authorities’ various methods of padding its figures to make them look much better. Noticeably after the Sino-U.S. trade war began in 2018, the statistical bureaus of various areas stopped releasing some key economic data and the NBS used the excuse of “calculating according to a comparable caliber” to massage its figures. The NBS’s “comparable caliber” is the reason why the year-on-year growth rate for the latest data is usually better than what it should be when compared with the central statistical bureau’s own data from the previous year.

To cover up economic contraction, the CCP authorities included China government bonds and local government general bonds when calculating total social financing from December 2019. The CCP authorities have also taken to restricting overseas access to sensitive information such as patents, statistics, business registration information, procurement documents, and academic journals in March 2023.

3. Beijing’s lifting of all restrictions on foreign investment in manufacturing is another indirect sign that the Chinese economy is declining rather than growing. For one, the fact that the CCP is willing to let foreigners freely invest in manufacturing rather than allow state-owned enterprises to maintain their monopoly and keep away “outsiders” suggests that the sector is struggling to generate profits.

China’s manufacturing sector started to face setbacks following the gradual shrinking of international demand after the 2007-2008 global financial crisis. After Xi Jinping took office, Beijing unveiled the “Belt and Road Initiative” in 2013 and so-called “supply-side structural reform” in 2015 partly as a way to address China’s overcapacity problems.

China’s manufacturing sector problems would further deepen with the Sino-U.S. trade war and U.S. efforts to “decouple” and “derisk” from China that started during the Trump administration and continued under President Joe Biden. The Biden administration’s measures restricting the PRC’s access to advanced technologies and promotion of “friendshoring” (i.e. shifting of production to friendly nations and away from geopolitical rivals) have also hastened the relocation of supply chains and manufacturing capacity out from the mainland. With geopolitical pressures compounding the problems already plaguing China’s manufacturing sector, the Xi leadership has no choice but to open up the sector to foreign investment as part of a broader effort to stabilize the Chinese economy’s rapid decline and better manage expectations at home and abroad.

4. The CCP’s padded economic data and propaganda do not appear to have restored investor confidence in the Chinese economy and its prospects. On Oct. 20, the Shanghai Composite Index fell below the major psychological level (typically seen as a dividing line between a “bull” and a “bear” market) of 3,000 points in early trading and closed at 2983.06 points. Mainland media also reported that foreign investors sold about 31.65 billion yuan of Chinese stocks through the northbound investment channel between Oct. 13 to Oct. 20.

Foreigners are not just pulling out of the Chinese stock market. On Oct. 20, the PRC Ministry of Commerce reported that actualized foreign investment fell 8.4 percent in the first nine months from a year ago to 919.97 billion yuan. This was the fourth consecutive month of declines, as well as an expansion of the decline.

China’s worsening economic prospects and growing geopolitical pressures aside, another reason for the acceleration of foreign capital outflows could be the yield on the benchmark 10-year U.S. Treasury threatening to stay above 5 percent. A further widening of the interest gap between the U.S. and China will make it more attractive for capital to exit the mainland and flow back to the United States.

5. We believe that the CCP no longer has any effective measures for rescuing the economy. Hence, Beijing can only rely on falsifying data and propaganda to keep up market confidence, sustain the CCP’s “great, glorious, and correct” image, and pursue its strategy of “delaying and waiting for change.”

When economic decline becomes too steep and rapid, however, the CCP authorities will likely run into hard limits on how much they can fake the data and churn out propaganda to maintain appearances and manage expectations about China’s economy.

2 PRC rolling over of local gov’t debt transfers risks to the banks

Oct. 6 to Oct. 20

ChinaBond.com, the website of the state-run China Central Depository & Clearing Co., Ltd., disclosed documents showing that 22 localities are preparing to issue a total of 943.78058 billion yuan worth of special refinancing bonds. The funds raised from these special refinancing bonds will be used to pay off implicit debt items like government arrears, loans, and non-standard debt; the funds from ordinary refinancing bonds are typically used to repay the principal on mature government bonds.

Oct. 17

Reuters reported that the PRC is asking state-owned banks to roll over existing government debt with longer-term loans at lower interest rates, citing two sources with knowledge of the matter.

The sources said that the People’s Bank of China gave orders in the week of Oct. 9, 2023 to major state lenders to extend terms, adjust repayment plans, and reduce interest rates on outstanding loans to local government financing vehicles (LGFVs). Loans that were due in 2024 or earlier will be classified as “normal” instead of non-performing if they are overdue, and those loans will not impact banks’ performance evaluations, one of the sources said. The sources did not say how much of the debt would be restructured.

One source said that interest rates on rolled over loans should not be below China’s Treasury bond rates (at the time of writing, the 10-year government bond yield was about 2.7 percent and the benchmark one-year loan rate was 3.45 percent) so that banks will not incur heavy losses from the debt restructuring. The source also said that the loan terms should not exceed 10 years.

The two sources said that the PBoC will set up an emergency tool with banks to offer loans to LGFVs to solve any short-term liquidity stress. A second source said that the LGFVs will have to repay the loans within two years.

A banker told Reuters, “The borrowing costs of LGFVs’ loans are usually about 4 percent, and in some regions and cases the costs could be even higher at about 5 percent to 8 percent. A large-scale loan extension and interest rate reduction will deal a heavy blow to banks’ operations.”

Reuters also cited a UBS research note as saying that LGFVs face significant bond maturity pressure in 2023 and in the first half of 2024. The note added that LGFVs are facing the highest maturity pressure in history, with over 2.1 trillion yuan of LGFV bonds maturing in the first half of 2023, another 1.75 trillion yuan in the second half of 2023, and 1.69 trillion yuan in the first half of 2024.

Reuters sources said that the PBoC will prioritize addressing debt risks in 12 regions identified as “high risk,” including Tianjin, Guizhou, and Guangxi, with a focus on open market bonds and non-standard debt products due in 2023 and 2024.

Oct. 19

The Wall Street Journal’s chief economic commentator Greg Ip argued in a column that a financial crisis is “no longer unthinkable” in China.

Ip wrote that an “imminent meltdown like the global panic that followed Lehman Brothers’ failure in 2008” is “highly unlikely,” but “China’s fiscal and financial imbalances are so large that they have taken the country—and, because of its size, the world—into uncharted territory.”

Ip cited data from the International Monetary Fund showing China’s slowing growth but swelling debt size, and noted that it is now “far harder” for China to “grow out of its debts than when growth was 10 percent, over a decade ago.” He added that the local governments borrowing heavily via LGFVs to fund urban development projects is a problem, and that the liabilities of local governments “now equal 45 percent of GDP.”

Ip observed that local governments are struggling to service their debts as land sales, “a primary source of revenue,” dried up, and cited an IMF estimate that 30 percent of LGFVs are “non viable without government support.” He added that this is a “big problem for China’s banks, which hold roughly 80 percent” of LGFV debt. Ip wrote, “Just half the cost of restructuring that debt would saddle them with impairment charges of $465 billion—chopping 1.7 percentage points off the ratio of loss-absorbing capital to assets, the IMF estimates.”

Ip further cited an observation from Rhodium Group’s director of China research Logan Wright that “financial crisis in China wouldn’t originate with an external shock or sudden revaluation of assets to reflect lower market prices. Instead it would happen when investors who assumed the government stood behind their assets learn that it doesn’t.”

Oct. 20

Mainland media 21st Century Business Herald reported that China’s financial system, and especially the banks, have recently started to support the resolution of local debt. The report said that banks’ participation in local debt resolution is broadly categorized into two scenarios, namely, the extension of interest rate reductions on bank loans and debt replacement.

The report said mature LGFV bonds and some non-standard debt will be the key replacement targets in the new round of debt resolution. With regard to fiscal debt, local governments can issue special refinancing bonds to pay off high-interest non-standard and LGFV bonds (that are considered as implicit debt). With regard to financialized debt, the regulatory authorities encourage banks to issue new loans to replace LGFV bonds and non-standard debt.

21st Century Business Herald cited Yuan Haixia, the executive director of China Chengxin International Research Institute, as estimating that commercial banks would be able to handle debt restructuring in the scale of 6 trillion yuan to 10 trillion yuan, but the actual scale of debt will be much lower than estimated. Yuan also said that debt restructuring essentially transfers risks from enterprises to commercial banks, and the regulatory indicators of those banks will deteriorate in the short term.

The 21st Century Business Herald report said that major state-owned banks will be the “main force” in the new round of debt roll overs because small- and medium-sized banks were overly involved in the municipal investment business in the last round of debt swaps. The report added that new risks have emerged from municipal investment assets with the current pressure on fiscal debt in some places, and cited the minutes of a meeting with regulatory authorities of an unspecified southern Chinese city as showing local government debt comprising a large proportion of loans issued by local small and medium-sized banks.

The report further noted that small and mid-sized banks have trouble striking a balance between meeting local debt requirements and achieving profitability due to higher funding costs. A source from the assets and liabilities department of a joint-stock bank in a western Chinese province told 21st Century Business Herald that the bank can “maintain original loans at the most” and the major state-owned banks will have to “pick up” the issuing of additional loans.

Backdrop

Several local governments have made public their debt and fiscal crises this year. These governments also indicated that they are unable to resolve their financial and debt problems, partly as a means to get the central government’s attention and support.

Our take

1. The news items above are more warning signs that the local government debt crisis is very severe and the central government is scrambling to avoid defaults. Local government debt defaults will inevitably trigger bigger problems that will have serious financial and political consequences for the CCP regime.

Other notable warning signs this year include:

- On Aug. 18, mainland media reported a relevant person in charge of the China Securities Regulatory Commission calling for the strengthening of monitoring and early warning of risks of LGFV bonds. The relevant person in charge also said that the top priority was making open market bonds and non-standard bonds “default proof,” and every effort should be made to maintain the smooth operation of the bond market.

- The “Minutes of a Meeting of Kunming City Investment Bond Experts” circulated in May 2023 disclosed that:

- Kunming has more than 20 billion yuan worth of LGFV bonds maturing in the second half of 2023. Kunming is now facing debt pressure from the open market and its non-standard debts are basically overdue. Also, there are too many debtors in Kunming and the situation is tough to handle, with the possibility of “all the pieces [LGFV debt risks] blowing up [defaulting].”

- The Yunnan provincial authorities requested at the start of the year that there cannot be any material default on public debt.

We wrote in the June 1, 2023 newsletter that “An official public default by a local government or that of an LGFV could lead to a concentration of successive defaults and technical defaults. This would in turn trigger the CCP regime’s systemic financial risks, negatively impact investor confidence, and spark an exodus of foreign capital from China.”

Beijing is undoubtedly aware of the dire consequences of allowing local governments to publicly default on their debt. Hence, the central government is now taking action to prevent defaults even though it has repeatedly called for “adhering to the principle of no assistance from the central government” and “parents should carry their own children” [誰家的孩子誰抱]). We currently believe that it is a matter of when, not if, some local governments default on their debt; whether or not the default becomes public knowledge is another question.

2. The various measures (roll overs, interest rate cuts, debt swaps, etc.) that the CCP has signaled that it would use to stabilize the local government debt situation only serve to delay repayment and avoid immediate defaults. While the banks technically do not hold non-performing loans, the scale of local government debt remains unchanged.

If anything, the size of local government debt will only balloon even more. A Goldman Sachs estimate puts local government debt, including the liabilities of LGFVs, at 94 trillion yuan (about $13 trillion). Assuming an interest rate of 5 percent, local governments are collectively due 4.7 trillion yuan in interest each year, or the equivalent of 31 percent of the national general public budget revenue from January to August 2023 (15.1796 trillion yuan).

As we previously noted, the CCP authorities’ effort to roll over debt merely transfers “debt risks to financial institutions” and does not actually resolve the regime’s broader financial troubles.

3. The 21st Century Business Herald report affirms our earlier observation that local governments are reliant on small and medium-sized banks for financing. The worsening of the local government debt problem means that small and mid-sized banks in China are facing substantial financial risks.

The risks of small and medium-sized banks are set to go up with the central government requiring banks to provide liquidity to local governments via long-term loans with low interest rates. While the 21st Century Business Herald piece states that major state-owned banks will be the “main force” in the upcoming debt roll overs, we believe that local governments will continue to rely on small and medium-sized banks for their financing needs. Such behavior would be characteristic of CCP officials, who tend to be narrowly focused on securing their political achievements and have few qualms about taking measures to save their skin but leave the crisis to their successors to resolve.